US stocks finished higher on Wednesday after a volatile session dominated by reports that President Trump was preparing to fire Federal Reserve Chair Jerome Powell. The S&P 500 and Dow Jones both recovered from earlier losses after Trump publicly denied the move, though investor anxiety remained elevated. Traders digested mixed earnings from major banks and chipmakers alongside fresh inflation data and tariff commentary. Meanwhile, the Nasdaq posted another record close, extending its year-to-date lead as strength in select tech names offset broader caution. Uncertainty around monetary policy leadership and the broader economic impact of tariffs continued to cloud the near-term outlook.

Key Takeaways:

- Dow Rebounds After Sharp Intraday Drop: The Dow Jones Industrial Average rose 231.49 points, or 0.53%, to finish at 44,254.78, reversing a steep 264-point dip earlier in the session. The bounce came after President Trump denied reports he was imminently firing Fed Chair Jerome Powell, though investor sentiment remained fragile.

- S&P 500 and Nasdaq Close Higher: The S&P 500 gained 0.32% to end at 6,263.70, while the Nasdaq Composite rose 0.26% to 20,730.49, marking its ninth record close this year. Early declines were swiftly recovered after Trump downplayed plans to remove Powell, helping sentiment stabilise. Chip stocks lagged, but strength in banks and large-cap tech offset broader sector rotation.

- European Markets Weaken Amid Powell Tensions and UK Inflation: European equities closed broadly lower as initial optimism gave way to concerns over Fed leadership and macroeconomic uncertainty. The Stoxx 600 fell 0.6%, led by a 2.2% decline in tech. France’s CAC 40 lost 0.6%, Germany’s DAX dipped 0.2%, and Italy’s FTSE MIB fell 0.4%, while the UK’s FTSE 100 slipped 0.13%. UK inflation surprised to the upside at 3.6% in June, with core CPI climbing to 3.7%, raising expectations that the Bank of England will maintain restrictive policy despite faltering growth. Meanwhile, Diageo pared earlier gains and Renault extended losses after cutting guidance. Richemont delivered stronger-than-expected sales, but overall market tone remained cautious due to tariff concerns.

- Asian Stocks Mostly Decline Despite Indonesia Trade Boost: Asia-Pacific markets were largely lower on Wednesday, pressured by weak trade data and global macro tensions. South Korea’s Kospi led declines, dropping 0.9%, while Japan’s Nikkei 225 closed flat. Australia’s ASX 200 lost 0.79%, and China’s CSI 300 fell 0.3%. South Korea reported falling export and import price indices alongside an unexpected dip in unemployment. Indonesia’s Jakarta Composite bucked the trend, rising 0.26% after Trump announced a preliminary trade agreement with Jakarta, including a new 19% export tariff. Still, caution prevailed across the region amid concerns over the broader economic fallout from US tariff actions.

- Wholesale Inflation Flat as Mortgage Demand Plunges: US producer prices were unchanged in June, falling short of expectations for a 0.2% gain. While core goods prices rose 0.3%, weakness in services offset gains, and the headline PPI rose 2.3% year-over-year. Analysts warned the data understates tariff effects, which could still feed into consumer prices. At the same time, mortgage application volume sank 10% last week as the average 30-year fixed rate rose to 6.82%, the highest in months. The combination of elevated inflation, higher borrowing costs, and political uncertainty weighed on housing demand and consumer confidence.

- Short-Term Treasury Yields Drop on Powell Speculation: The 2-year Treasury yield slid 6 basis points to 3.896% on Wednesday, as markets priced in the risk of sudden leadership change at the Fed. The 10-year yield also declined modestly to 4.459%, while the 30-year held near 5.014%. The move reflected a flight to safety and potential reassessment of rate path expectations if Powell were removed.

- Oil Slips Despite Strong Demand Signals: Brent crude edged down 0.07% to settle at $68.76, while WTI crude fell 0.23% to $66.67. Gains were capped by a surprise build in US gasoline and distillate inventories, which offset a larger-than-expected draw in crude stockpiles. Gasoline stocks rose by 3.4 million barrels and distillates by 4.2 million, far exceeding forecasts. The data raised doubts over near-term consumption strength, even as broader demand trends remain constructive.

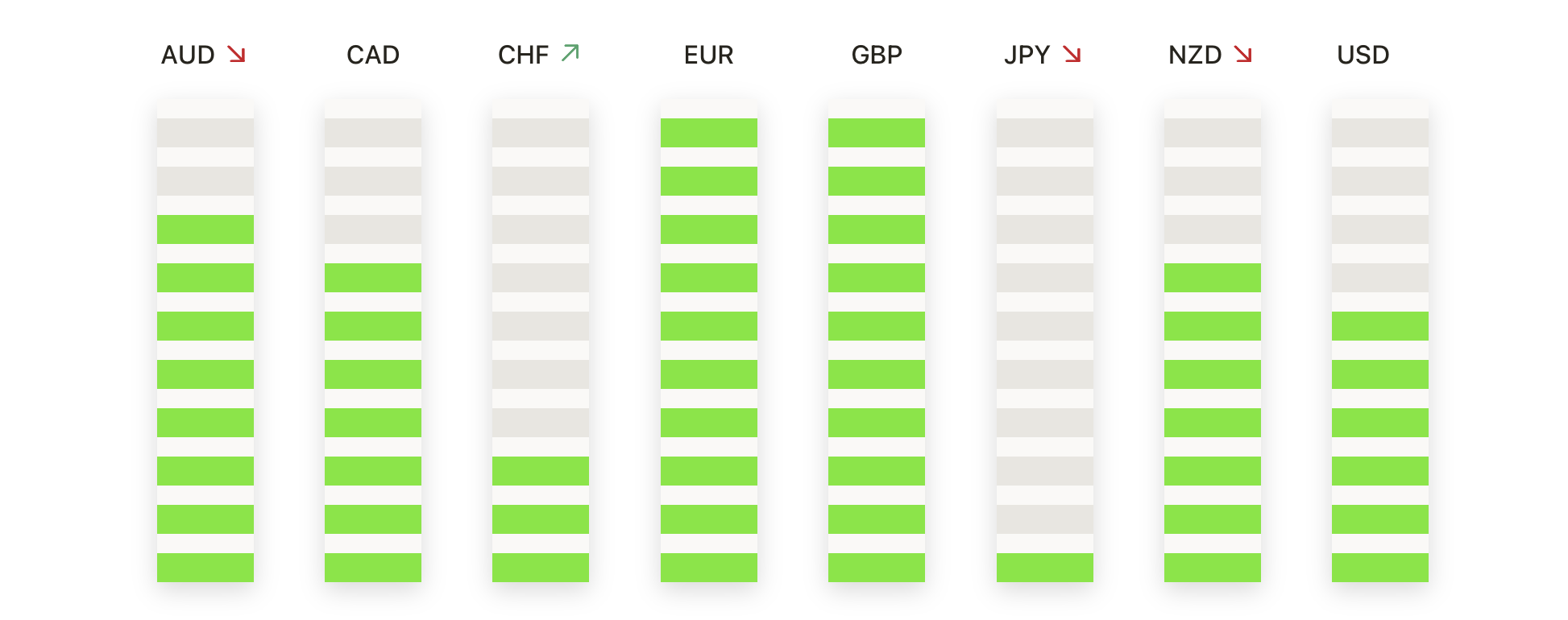

FX Today:

- EUR/USD Snaps Losing Streak Near 1.1600: The EUR/USD pair closed at 1.1634, rising 0.28% after rebounding from a low of 1.1566 and reaching a high of 1.1722.. Price continues to trade comfortably above the 50-day SMA at 1.1484, reinforcing the broader uptrend that has remained intact since mid-April. While the session ended well below the intraday high, indicating some late-session hesitation, EUR/USD continues to hold above all major moving averages. Resistance is now seen at 1.1750 and 1.1800, with near-term support at 1.1550 followed by the 50-day average. The pair remains in a short-term corrective phase but is still technically bullish as long as price holds above 1.1500.

- GBP/USD Holds 1.3400 After Steep Five-Day Drop: The GBP/USD pair closed at 1.3416, gaining 0.23% after bouncing off a session low of 1.3366. Cable printed a modest green candle, breaking a five-day losing streak that wiped out the early July rally. Despite the rebound, the pair remains capped below the 50-day SMA at 1.3502, which has turned into immediate resistance. The 100-day and 200-day SMAs continue to slope upward, offering longer-term support at 1.3274 and 1.2961 respectively. A sustained move above 1.3550 is needed to revive bullish momentum, while failure to reclaim 1.3500 may invite another push toward the 1.3300 handle.

- USD/JPY Retreats Sharply After Hitting Key Resistance: The USD/JPY pair settled at 147.86, falling 0.65% after reaching an intraday high of 149.19. The pair printed a bearish engulfing candle, marking the first decline in six sessions and reflecting a sharp rejection from the 200-day SMA near 149.60. Momentum shifted decisively lower after the failed breakout attempt, with the session closing near the low of the day at 146.91. Despite this drop, the broader structure remains improved as price still holds above both the 50-day and 100-day SMAs, located at 145.06 and 145.78. If the pair breaks below 146.50, it could open the door for a move toward 145.00. A rebound above 149.60 is required to retest resistance in the 150.50 to 151.00 region.

- USD/CAD Rejected at 50-Day Average Yet Again: The USD/CAD pair ended at 1.3686, slipping 0.26% after peaking at 1.3756 and dipping to a low of 1.3680. The pair posted a red candle after Tuesday’s recovery, with price again struggling to sustain gains above the descending 50-day SMA, now at 1.3738. Although the pair has stabilised around the 1.3600 to 1.3700 area, every rally attempt has been met with selling pressure. Bears remain in control unless the pair breaks above 1.3750, which could shift short-term sentiment and trigger a move toward 1.3850. On the downside, a breach of 1.3630 would increase the risk of retesting the yearly low near 1.3500.

- Gold Rebounds from Intraday Low but Stalls Below $3,350: Gold settled at $3,347 on Wednesday, advancing 0.70% after dipping to a low of $3,319 and hitting a high of $3,377. The price briefly tested the $3,380 area and it failed to close above the key $3,350 level. The metal remains above its 50-day SMA at $3,325, with support also seen around the $3,320 mark. Longer-term SMAs, including the 100-day and 200-day at $3,205 and $2,953 respectively, confirm the broader uptrend is still in place. Without a breakout above $3,380 to $3,400, price action is likely to remain range-bound in the short term.

Market Movers:

- Tesla Jumps on Risk-On Rotation: Shares of Tesla gained more than 3.5% as the stock led gains among the Magnificent Seven.

- Amazon Slips Despite Stable Revenue Outlook: Amazon fell 1.4% on Wednesday, underperforming peers as investors locked in profits following a strong run.

- Goldman Sachs Rises on Record Trading Revenue: Goldman Sachs closed up 0.9% after posting a record $4.3 billion in equity-trading revenue. Strong performance in asset and wealth management also supported the upside, with management fees up 11% year-on-year.

- Bank of America Dips After Earnings Beat: Bank of America slipped 0.3% despite reporting better-than-expected net interest income and strong trading results. Investors appeared to focus on forward guidance, which included cautious commentary on credit quality.

- Morgan Stanley Falls on Weaker Sentiment: Morgan Stanley ended down 1.3% even after reporting strong equity-trading income and growth in wealth management assets. Concerns over broader revenue trends weighed on investor reaction to the solid results.

- ASML Sinks on Cautious Outlook: Shares of ASML plunged more than 8% after the company issued subdued guidance for the coming year.

- Crypto Stocks Rally with Bitcoin Surge: Cryptocurrency-exposed stocks advanced as bitcoin gained 2.3% on optimism around a new pro-crypto bill. Riot Platforms, Marathon Digital, and MicroStrategy all closed more than 3% higher as traders bet on regulatory progress.

Markets closed higher on Wednesday after a volatile session marked by speculation over Fed leadership and lingering tariff uncertainty. While President Trump’s denial of plans to fire Jerome Powell helped calm equities, traders remained alert to political risks and inflation trends. Bank earnings and chip sector weakness added to the mixed tone, though the Nasdaq continued to edge higher. European and Asian markets were broadly lower, and fresh UK inflation data reinforced expectations for tighter monetary policy. Looking ahead, investors will focus on upcoming corporate results and any fresh signals from central banks, with political headlines likely to remain a key market driver.