US equities climbed sharply on Monday as buyers stepped back in after last week’s sell-off, with strength in technology and semiconductor shares driving gains across all major indices. Investors appeared willing to put aside recent concerns over softer economic data and fresh tariff measures, focusing instead on the potential for progress in trade discussions and an upbeat start to the week’s corporate earnings calendar. The rebound came as markets entered a seasonally challenging month, with August often associated with increased volatility and lighter trading volumes.

Key Takeaways:

- Dow Rebounds Sharply: The Dow Jones Industrial Average climbed 585.06 points, or 1.34%, to 44,173.64, fully erasing Friday’s sharp losses. The move marked one of the Dow’s strongest single-day advances in recent months, as investors engaged in broad-based buying.

- S&P 500 Posts Best Day Since May: The S&P 500 advanced 1.47% to 6,329.94, snapping a four-day losing streak in a decisive rebound. The index’s performance underscored renewed risk appetite at the start of August, despite its historically poor track record for the month.

- Nasdaq Leads Gains: The Nasdaq Composite surged 1.95% to 21,053.58, outperforming the other major indices. Large-cap tech names such as Nvidia, Alphabet, and Meta Platforms gained over 3%, while Microsoft and Tesla advanced more than 2%, boosting the sector-heavy index.

- Europe Markets End Broadly Higher Despite Swiss Weakness: European equities advanced in a generally positive session, with the Stoxx Europe 600 closing 0.8% higher. The FTSE 100 rose 0.66% to 9,128.30, the CAC 40 climbed 1.06%, the FTSE MIB jumped 1.89%, and the DAX gained 1.42%. Swiss stocks lagged, with the Swiss Market Index down 0.2% after the US imposed 39% tariffs on the country. Economic data was mixed, as German engineering orders fell 5% year-on-year in June on weaker demand both domestically and abroad, while Spain’s unemployment edged down 0.1% in July to its lowest since 2008, with total employment reaching 21.64 million. Sentiment was lifted by news that the EU will delay for six months its planned countermeasures to US tariffs following a late-July agreement between President Ursula von der Leyen and President Trump, aimed at restoring stability for businesses across both regions.

- Asia Markets Mixed as Investors Weigh Tariffs and Oil Supply Moves: Asia-Pacific markets saw a varied performance, with Hong Kong’s Hang Seng up 0.92% and China’s CSI 300 higher by 0.39%. South Korea’s Kospi gained 0.91% and the Kosdaq rose 1.46%, while India’s Nifty 50 and Sensex added 0.49% and 0.42% respectively. Japan lagged, with the Nikkei 225 falling 1.25% and the Topix down 1.10%. Australia’s ASX 200 was flat, and markets in Jakarta and Kuala Lumpur slipped over 0.3%. Investors balanced ongoing US tariff updates with the OPEC+ decision to raise output from September.

- Oil Prices Drop on OPEC+ Output Hike: Brent crude settled 1.31% lower at $68.76 a barrel, while WTI fell 1.54% to $66.29. The declines followed OPEC+’s agreement to boost production by 547,000 barrels per day in September, completing the reversal of its largest supply cuts. The move was in line with expectations but came amid continued geopolitical risks, particularly around potential sanctions on Russia.

- Treasury Yields Steady as Economic Concerns Linger: The 10-year Treasury yield edged down over 2 basis points to 4.198%, the 30-year slipped less than 2 basis points to 4.795%, and the 2-year fell 1 basis point to 3.694%. Yields held firm despite remaining concerns from last week’s weak jobs report, which saw May and June payrolls revised down by a combined 258,000.

- US Factory Orders Decline Sharply: New orders for US-manufactured goods fell 4.8% in June, matching forecasts and reversing May’s upwardly revised 8.3% jump. The drop was driven by a sharp fall in commercial aircraft orders, while year-on-year orders rose 3.8%. Manufacturing remains constrained by elevated tariffs, with the ISM manufacturing index slipping to a nine-month low in July.

FX Today:

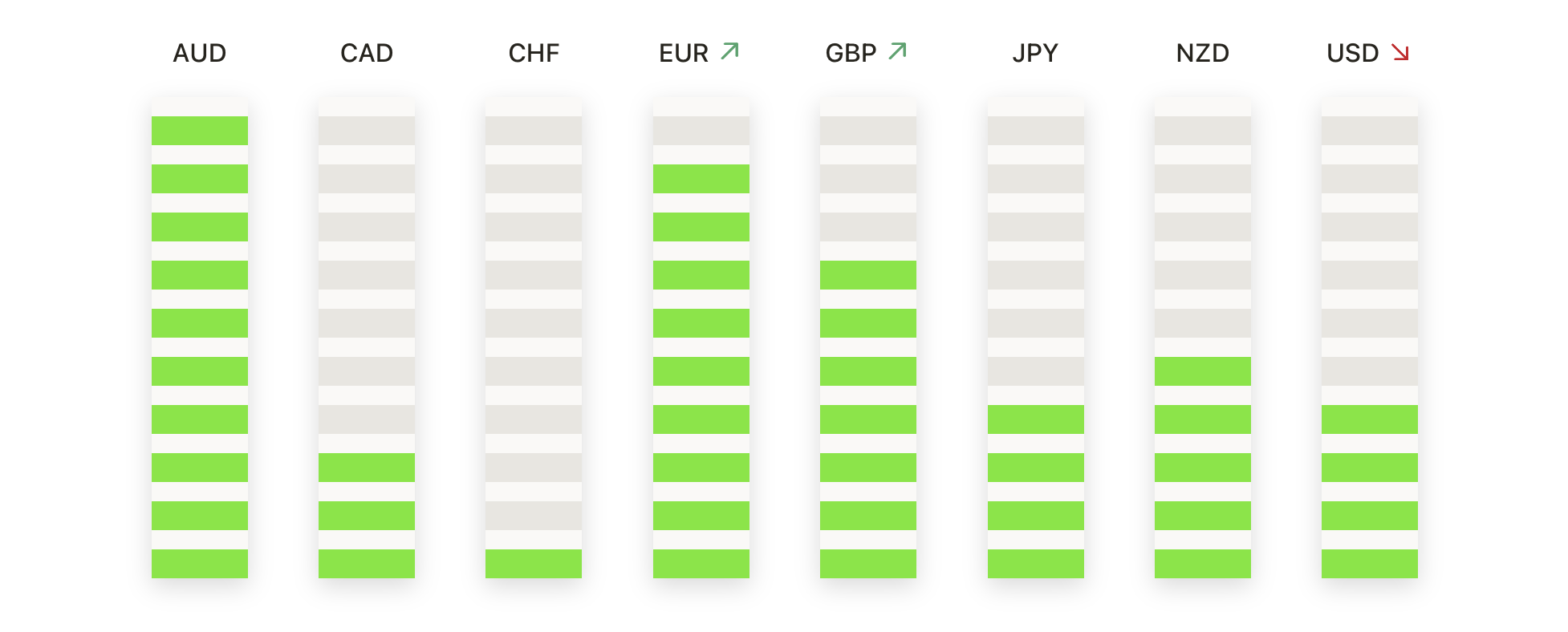

- EUR/USD Holds Range as Buyers Lose Momentum: EUR/USD closed at 1.1568, down 0.15% after touching a high of 1.1595 and finding support at 1.1540. The daily candle formed a narrow body, signalling indecision as price held just below the 50-day SMA at 1.1582 and above the 100-day SMA at 1.1371. The medium-term trend remains constructive, but the pullback from July highs has shifted focus to the 100-day SMA, which held firmly last week. The recovery from 1.1400 has stalled at the 50-day SMA, making this level a key pivot. Resistance is layered at 1.1620 and 1.1700, while support lies at 1.1500 and 1.1400. A daily close above 1.1620 could reignite bullish momentum toward 1.1700, but a drop below 1.1500 would expose 1.1400 and potentially trigger a deeper retracement toward the 200-day SMA at 1.0946.

- GBP/USD Consolidates Near Support After Steep Drop: GBP/USD ended at 1.3276, down 0.02% after ranging between 1.3331 and 1.3254. The session produced a small-bodied doji, reflecting consolidation after Friday’s sharp decline, with price holding below the 50-day SMA at 1.3511 and the 100-day SMA at 1.3345, and only marginally above the 200-day SMA at 1.2988. Consolidation above 1.3200 suggests a temporary pause rather than a reversal, as downside pressure persists while price trades under converging short- and medium-term averages. Immediate resistance is at 1.3345 where the 100-day SMA meets recent swing highs, while support rests at 1.3200 and 1.3100. A close above 1.3345 would ease selling pressure, but failure to hold 1.3200 risks a move toward 1.3100 and potentially the 200-day SMA.

- USD/CHF Recovery Slows Under Key Moving Averages: USD/CHF settled at 0.8082, up 0.61% after trading between 0.8010 and 0.8097. The session delivered a firm-bodied gain, extending Friday’s bounce from the 0.8000 floor, yet price remains well beneath the 50-day SMA at 0.8069 and the 100-day SMA at 0.8245, keeping the broader downtrend intact. While short-term momentum has improved, the falling medium-term averages suggest sellers may return. Resistance is at 0.8100 and then 0.8200, where a sustained break could shift focus to the 200-day SMA at 0.8589. On the downside, 0.8000 remains the key support, with a break exposing 0.7900 and extending bearish bias.

- Gold Targets $3,400 After Extending Recovery: Gold closed at $3,375, up 0.39% after trading between $3,345 and $3,385, marking its second consecutive gain following last week’s drop to $3,280. Price is now holding above the 100-day SMA at $3,263 and testing the 50-day SMA at $3,342 from above, reinforcing the short-term recovery. The broader trend remains supported by higher lows since March and the 200-day SMA at $2,999. July’s double rejection at $3,440 remains the key upside barrier, with intermediate resistance at $3,400. A sustained close above $3,400 would open a retest of the $3,440–$3,480 zone, while failure to clear it could prompt a retreat toward $3,340–$3,300.

- Silver Pushes Higher but Still Faces Resistance: Silver ended at $37.38, up 0.97% after ranging between $36.68 and $37.47. The move extended the rebound from last week’s low, with the 50-day SMA at $36.46 holding as immediate support. The broader uptrend stays intact above the 100-day SMA at $34.61 and 200-day SMA at $32.97. The current advance is testing the underside of a short-term descending channel from mid-July, making $38.00 a key pivot. Above this, resistance is at $38.60 and then the July high at $39.20, where sellers previously emerged. A close above $39.20 would re-establish bullish control toward $40.00, while failure to break $38.00 could see a drift back toward $36.50.

Market Movers:

- Palantir Surges on Record Revenue and Upgraded Outlook: Shares jumped nearly 5% after hours, having closed up 4%, as Palantir posted over $1 billion in quarterly revenue for the first time and raised its full-year guidance above expectations.

- Tech Giants Lift Broader Market: Nvidia, Alphabet, and Meta Platforms gained more than 3%, Microsoft and Tesla rose over 2%, and Apple added 0.48%, with chipmakers including Broadcom, KLA Corp, and AMD also providing strong support.

- Idexx Labs Leads Index Gainers on Earnings Beat: Stock surged more than 27% after Q2 revenue of $1.11 billion topped forecasts, and the company raised its full-year EPS outlook to as much as $12.76 from a prior $12.43 high.

- Wayfair Rallies on Stronger-Than-Expected Profit: Shares rose more than 11% as adjusted Q2 earnings came in at $0.87 per share, comfortably above the $0.33 consensus estimate, signalling improved operational efficiency.

- Spotify Gains on Subscription Price Increases: Stock advanced more than 5% after announcing premium subscription price hikes across South Asia, the Middle East, Africa, Europe, and Latin America.

- ON Semiconductor Drops on Weak Margin Forecast: Shares fell over 16%, leading S&P 500 and Nasdaq 100 decliners, after projecting Q3 adjusted gross margin midpoint of 37.5%, below analyst expectations.

US equities began the week on a strong note, with major indices reversing much of the prior session’s losses as technology and semiconductor stocks fuelled broad-based gains. Optimism in Europe was underpinned by a delay in EU tariff countermeasures, while Asia delivered a mixed performance amid ongoing trade and supply considerations. Commodity markets reflected the impact of fresh OPEC+ output plans, with oil prices easing, while precious metals extended their recoveries. In currencies, major pairs held within well-defined ranges, signalling caution ahead of key resistance levels. With a relatively light economic calendar, attention now shifts to corporate earnings and any fresh developments in US-China trade talks, both of which are likely to set the tone for the remainder of the week.