The S&P 500 surged to another record high on Monday as Nvidia’s $100 billion investment plan in OpenAI reignited excitement around artificial intelligence. While stocks opened lower, gains in big tech, including Apple and Oracle, powered markets back to fresh highs across all three major indexes. Political risk in Washington around a looming government shutdown capped broader sentiment, but the AI-fuelled rally proved strong enough to keep momentum firmly on the upside.

Key Takeaways:

- Dow Jones Inches Higher: The Dow Jones Industrial Average climbed 66.27 points, or 0.14%, to finish at 46,381.54. The index touched a record intraday peak before settling higher but trailed the broader market as cyclical sectors underperformed and political uncertainty tempered enthusiasm.

- S&P 500 Extends Record Run: The S&P 500 advanced 0.44% to 6,693.75, securing another record close. Nvidia led gains with a 3.9% jump on news of a $100 billion OpenAI investment, while Oracle surged after a leadership reshuffle and Apple rallied on strong iPhone sales. The index remains supported by expectations for further Fed cuts this year.

- Nasdaq Rises on Tech Strength: The Nasdaq Composite added 0.70% to 22,788.98, outperforming as technology names dominated trade. Oracle climbed 6% after naming new co-CEOs, while Apple jumped 4% on fresh optimism for its latest iPhone cycle. Nvidia’s surge confirmed that AI remains the key market driver.

- European Stocks Close Lower: The Stoxx 600 slipped 0.5% as auto stocks dragged the region lower. Germany’s DAX lost 0.48%, the CAC 40 fell 0.30%, and the Stoxx autos index dropped 1.9%. Porsche tumbled 7.2% after slashing its 2025 profit outlook and delaying EV launches, while Volkswagen shed 7.1% on the same news. The FTSE 100 outperformed, rising 0.11%, while Italy’s FTSE MIB added 0.3% as investors assessed rate impacts on its economy. Euro zone consumer confidence improved modestly, rising 0.6 points to -14.9, though ECB data showed consumers shifting spending away from US goods in response to tariff concerns.

- Asian Markets Diverge: India’s IT stocks slumped nearly 3% after Trump’s new $100,000 H-1B visa fee, with Mphasis, Persistent Systems, and LTIMindtree among the biggest losers. The Nifty 50 fell 0.49% and the Sensex dropped 0.56%. By contrast, Adani Power soared more than 15% on its stock split. China’s CSI 300 rose 0.46% after the PBoC kept loan prime rates steady, while Hong Kong’s Hang Seng slipped 0.76%. Japan’s Nikkei gained 0.99% and the Topix added 0.49% as yields hit 18-year highs. South Korea’s Kospi rose 0.68% with Samsung jumping 4% on HBM approval from Nvidia. Australia’s ASX 200 climbed 0.43%, highlighting the region’s mixed performance.

- Oil Prices Ease as Iraq Boosts Exports: Brent crude slipped 0.10% to $66.61 while WTI fell 0.06% to $62.64. Iraq increased exports to 3.4–3.45 million barrels per day under OPEC+, stoking oversupply concerns. Traders also weighed reports of possible Kurdish pipeline exports resuming via Turkey, offsetting geopolitical tensions in the Middle East and Eastern Europe.

- Treasury Yields Steady Ahead of Inflation Data: The 10-year Treasury yield rose to 4.149%, the 2-year climbed to 3.605%, and the 30-year inched up to 4.765%. Investors await Friday’s US personal consumption expenditures index, expected to show contained inflation and reinforce the Fed’s gradual approach after last week’s quarter-point cut.

FX Today:

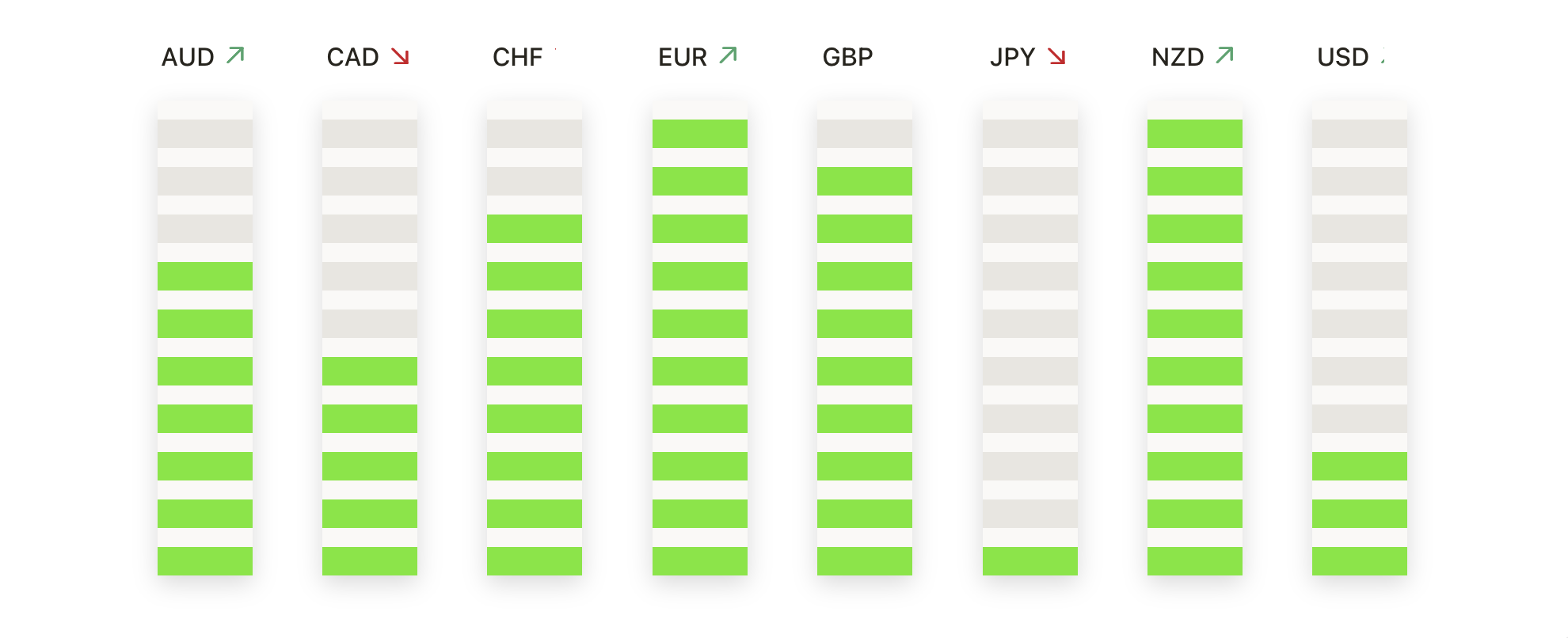

- EUR/USD Holds Above 1.1800 as Bulls Defend Breakout: EUR/USD closed at 1.1802, up 0.45%, after trading between 1.1726 and 1.1802. The pair ended near the high, confirming strong demand even after early volatility. It remains well supported above the 50-day moving average at 1.1670, alongside the 100-day at 1.1571 and the 200-day at 1.1132. The bullish trend since March remains intact, with higher lows reinforcing momentum. Key support now sits at 1.1700, with buyers protecting the breakout area. Upside targets remain 1.1885–1.1900, where a sustained close would open the door towards the psychological 1.2000. A failure back under 1.1725 would undermine the breakout and risk a deeper pullback to the 50-day average, but for now bulls are in control.

- GBP/USD Steadies After Pullback: GBP/USD settled at 1.3518, up 0.35%, after a session between 1.3453 and 1.3521. The pair printed a small-bodied candle, showing consolidation after rejection from last week’s highs above 1.3700. It is holding above the 50-day average at 1.3467 and the 100-day at 1.3483, with the broader trend supported by higher lows since August. Immediate resistance stands at 1.3620 and then 1.3700, where sellers capped the last advance. A decisive close above would renew bullish control, while a break under 1.3450 risks exposing 1.3350. With moving averages converging, this is a key inflection zone for near-term direction.

- USD/CAD Climbs Back as Buyers Regain Ground: USD/CAD closed at 1.3822, up 0.37%, after trading from 1.3771 to 1.3822. The session extended the rebound from early September, holding above the 50-day at 1.3771 and testing the 100-day at 1.3759. The 200-day at 1.4003 continues to cap upside, defining the broader bearish tilt since April. Recent higher lows above 1.3700 suggest near-term stabilisation, but the pair must close above 1.3850 to build momentum towards 1.3950–1.4000. A slip back under 1.3770 would threaten a retest of 1.3700 and re-expose September’s lows. For now, buyers have short-term initiative but face heavy resistance overhead.

- USD/JPY Stays Below 148.00 as Consolidation Drags On: USD/JPY ended at 147.70, down 0.17%, with a range of 147.66 to 148.38. The tight range underscored the pair’s ongoing lack of momentum. It remains compressed between the 50-day at 147.69, the 100-day at 146.27, and the 200-day at 148.56. This sideways pattern reflects indecision, with lower highs since June balanced by higher lows since August. A break above 148.60–149.00 would reopen 150.00, while a close under 146.20 would hand control to sellers and target 145.00. For now, the market is stuck in consolidation awaiting a catalyst.

- Gold Surges to Record High as Bulls Stay in Control: Gold closed at $3,748, up 1.73%, after trading between $3,684 and $3,749. The strong bullish candle confirmed sustained upward momentum, with price firmly above the 50-day at $3,441 and the 100-day at $3,381. Successive higher lows since mid-year underpin the bullish structure, while the breakout through $3,700 adds fresh support. Immediate protection lies at $3,700 and $3,650, while resistance targets stretch towards $3,800 and higher. Only a close back under $3,700 would suggest a pause in the rally, but trend and momentum remain aligned higher.

- Silver Extends Rally to Fresh All-Time High: Silver settled at $44.08, up 2.37%, after trading from $43.05 to $44.11. The market ended at the session high, confirming buyer dominance. Price remains well supported above the 50-day at $39.25, with the 100-day at $36.98 and 200-day at $34.32 strengthening the long-term base. The breakout above $42.00 and $43.00 has driven fresh record highs, with immediate support now at $43.00 and $41.50. Bulls are targeting $45.00 and $46.00 as the next milestones, keeping momentum firmly in their favour.

Market Movers:

- Applied Materials Leads Semiconductors Higher: Shares rose more than 5% after Morgan Stanley upgraded the stock to overweight with a $209 target, lifting AI-infrastructure names across the Nasdaq 100.

- Chip Stocks Rally on AI Momentum: Lam Research, Seagate, and Western Digital all gained over 4%, while Nvidia advanced more than 3%. ASML, KLA, and Marvell added over 2%, with AMD, Micron, and Qualcomm also posting gains.

- Teradyne Surges on Analyst Upgrade: The stock jumped more than 12% after Susquehanna raised its price target to $200 from $133, making it the top gainer in the S&P 500.

- Apple Climbs on iPhone Optimism: Shares rose more than 4% to lead Dow gainers after Wedbush lifted its price target to $310, citing strong demand for the new iPhone lineup.

- MBX Biosciences Doubles on Trial Success: The biotech soared over 101% after its weekly canvuparatide treatment met the main goal in a Phase 2 study for chronic hypoparathyroidism.

- Metsera Jumps on Pfizer Takeover: Shares surged more than 61% after Pfizer agreed to buy the company for $4.9 billion, valuing it at $47.50 per share.

- Crypto Stocks Fall with Bitcoin: Shares of Coinbase, MARA, Riot, MicroStrategy, and Bit Digital each fell more than 2% after Bitcoin slipped to a 1.5-week low.

- Kenvue Slumps on Tylenol Report: The consumer health firm dropped over 7% after reports linked Tylenol’s active ingredient to autism, sparking regulatory concerns.

- Keurig Dr Pepper Drops on Downgrade: Shares fell more than 4% after BNP Paribas Exane cut its rating to underperform with a $24 target.

- Match Group Slides on Competition: The dating app company lost over 5% after Meta unveiled new Facebook Dating features designed to increase engagement.

Markets are increasingly defined by two opposing forces: surging optimism around artificial intelligence, which is pushing Wall Street to successive records, and persistent policy and political risks that continue to cloud the outlook. European and Asian moves highlighted how regional pressures, from Porsche’s downgrade to India’s visa-driven selloff, remain equally influential. With precious metals in record territory and inflation data due later this week, investors face a pivotal test of whether momentum can broaden beyond technology and carry global markets higher into the final quarter.