Wall Street extended its rally on Monday with the Nasdaq closing at a record high and the S&P 500 edging higher, setting the stage for a pivotal week dominated by US inflation releases. Gains were driven by strength in technology stocks, particularly chipmakers, while investors looked ahead to producer and consumer price data that could determine the Federal Reserve’s policy path later this month. Gold also surged to fresh all-time highs above $3,600, underlining strong demand for safe havens even as equity benchmarks trade at records. The combination of record-breaking moves in both tech shares and bullion reflected a market balancing optimism over growth with caution around policy and inflation trends.

Key Takeaways:

- Dow Jones Advances Modestly: The Dow Jones Industrial Average added 114.09 points, or 0.25%, to finish at 45,514.95, supported by strength in technology and consumer names.

- S&P 500 Edges Higher: The S&P 500 closed up 0.21% at 6,495.15, with broad-based gains across sectors reinforcing the market’s steady tone.

- Nasdaq Hits Fresh Record: The Nasdaq Composite rose 0.45% to a record close of 21,798.70, having also set a new intraday high, led by advances in Broadcom, Nvidia, Amazon, and Microsoft, underpinned by continued enthusiasm for AI and semiconductor demand.

- Europe Markets Gain Despite French Government Collapse: European equities advanced with the STOXX 50 up 0.9% and STOXX 600 higher by 0.6%. France’s CAC 40 rose 0.88% earlier in the day, though later Prime Minister François Bayrou’s government fell after losing a confidence vote by 364 to 194 over plans for €44 billion in budget cuts aimed at reducing the deficit to 4.6% of GDP in 2026. Germany’s DAX added 0.89% after industrial production grew 1.3% in July, beating expectations, though exports slipped 0.6% month-on-month as shipments to the US dropped 7.9%. Industrial orders fell 2.9% in July, marking a third straight monthly decline and highlighting underlying weakness. London’s FTSE 100 closed 0.14% higher, while Italy’s FTSE MIB gained 0.3%, rounding out a session that ended firmly in positive territory despite growing political and economic headwinds.

- Asia Markets Climb as Japan Faces Leadership Change: Asia-Pacific stocks ended mostly higher with Japan in focus after Prime Minister Shigeru Ishiba announced his resignation. The Nikkei 225 surged 1.45% to 43,643.81 and the Topix hit a record 3,138.2, lifted by optimism over potential successors such as Koizumi Shinjiro and Sanae Takaichi. Gains were reinforced by easing political uncertainty and prospects for pro-growth leadership. South Korea’s Kospi rose 0.45% and the Kosdaq gained 0.89%, while Hong Kong’s Hang Seng advanced 0.8%. China’s CSI 300 edged 0.16% higher after exports grew 4.4% year-on-year in August, though the figure fell short of expectations and import growth remained weak amid property sector strains. Australia’s ASX 200 slipped 0.24% as miners lagged, while India’s Nifty 50 and Sensex rose 0.44% and 0.34% respectively, continuing their steady upward momentum.

- Oil Prices Rebound: Brent crude gained 0.79% to $66.02 a barrel while WTI rose 0.63% to $62.26, bouncing from last week’s losses after OPEC+ announced a smaller-than-expected October output increase.

- Treasury Yields Ease After Last Week’s Highs: US bond yields pulled back on Monday, with the 10-year down more than 4 basis points to 4.044%, the 2-year slipping to 3.495%, and the 30-year dropping over 8 basis points to 4.689%. The move followed a sharp run-up in global yields last week, when Japan’s 30-year touched a record high, the UK’s 30-year reached its highest level in 27 years, and the US 30-year briefly climbed above 5% for the first time since July. The retreat reflects a cautious reset ahead of US inflation data due later this week, which could determine the Federal Reserve’s policy path.

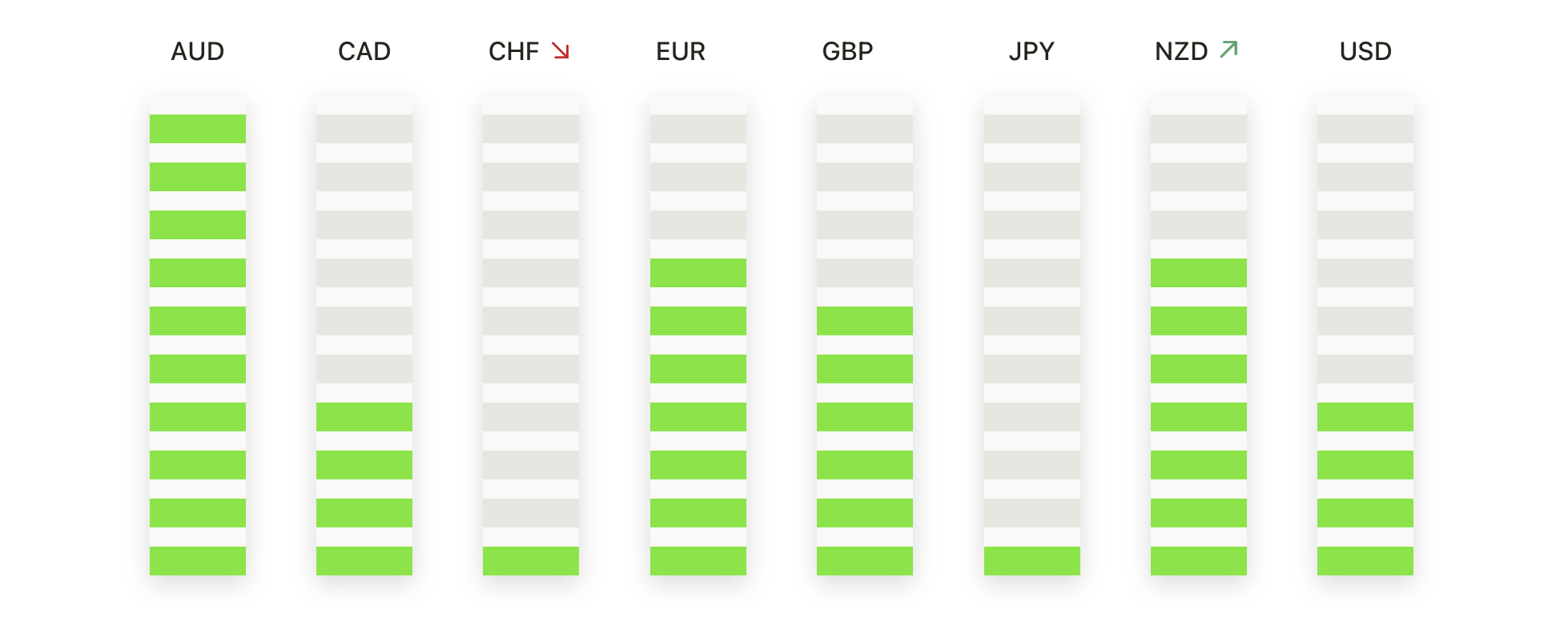

FX Today:

- EUR/USD Builds Momentum as Buyers Press Towards 1.1800: EUR/USD rose 0.37% to close at 1.1760 after trading between a high of 1.1766 and a low of 1.1704. The pair has been trending higher since early August, supported by aligned moving averages at 1.1664, 1.1530, and 1.1070. Resistance remains at 1.1800, a level that has capped rallies repeatedly since July, while support is found at 1.1700 and the 50-day average just below. A break above 1.1800 would open scope for 1.1900, while holding above 1.1700 keeps the bias firmly to the upside.

- GBP/USD Edges Higher as Resistance Comes Into Play: GBP/USD advanced 0.31% to finish at 1.3549 after posting a high of 1.3566 and a low of 1.3483, leaving a strong green candle that signalled renewed bullish control. The pair is pressing against the top of its consolidation range, underpinned by the 50-day at 1.3474, the 100-day at 1.3459, and the 200-day at 1.3070. The recovery from August’s 1.3350 low remains intact, with resistance now at 1.3566 and 1.3650 beyond. Support is set at 1.3480 and then 1.3400, keeping the overall structure constructive while price holds above key averages.

- USD/CHF Extends Decline as Break Confirms Bearish Bias: USD/CHF fell 0.59% to settle at 0.7931 after reaching a high of 0.7996 and a low of 0.7927. The pair is trading below all major moving averages, with the 50-day at 0.8016, the 100-day at 0.8117, and the 200-day at 0.8498, reflecting entrenched weakness. Sellers remain dominant after repeated failures above 0.8100 in August, leaving support at 0.7927 and scope for further downside towards 0.7850. Any rebound would face resistance at 0.8000 and 0.8050.

- USD/JPY Remains Range-Bound as Market Awaits Breakout: USD/JPY closed fractionally higher at 147.44, up 0.06%, after trading between 148.58 and 147.34. The pair has been locked in a sideways pattern since mid-July, unable to clear 149.00 on the upside or break below 146.00. Resistance stands at 148.60, with support at 146.80–147.00. A decisive move beyond this range would set the next trend direction, either towards 150.00 or back down towards 146.00.

- AUD/USD Climbs as Buyers Target Break Above 0.6600: AUD/USD gained 0.65% to settle at 0.6593 after posting a high of 0.6599 and a low of 0.6545. The pair has rebounded to the top of its consolidation zone, supported by the 50-day at 0.6519, the 100-day at 0.6487, and the 200-day at 0.6387. Buyers continue to defend the 0.6450–0.6500 area, keeping the short-term outlook constructive. Resistance is at 0.6599 and then 0.6650, while support lies at 0.6550 and the 50-day moving average.

- EUR/GBP Holds Firm as 0.8700 Level Limits Upside Progress: EUR/GBP closed 0.12% higher at 0.8679 after recording a high of 0.8684 and a low of 0.8662. The pair is holding above the 50-day at 0.8654, the 100-day at 0.8563, and the 200-day at 0.8463. Resistance remains at 0.8700, which has capped price since July, while support is at 0.8660 and then 0.8600. A close above 0.8700 would open scope towards 0.8750, but failure to break higher could extend the range.

- Gold Pushes Higher as Record Close Brings $3,700 Into View: Gold rallied 1.38% to end at $3,635 after trading between $3,646 and $3,578. The metal remains strongly supported above the 50-day at $3,373 and 100-day at $3,347, reflecting a powerful uptrend. The breakout above $3,600 has unlocked fresh buying interest, with resistance now at $3,646 and scope to target $3,700 if momentum continues. Support is seen at $3,600 and then $3,550.

Market Movers:

- Broadcom and Marvell Lead Chip Rally on AI News: Broadcom gained more than 3% after last Friday’s 9% surge, while Marvell Technology jumped over 3% as reports of a partnership with OpenAI lifted demand across the sector. Lam Research added more than 2%, ASML rose over 1%, and Nvidia and Analog Devices also advanced.

- AppLovin Climbs on S&P 500 Inclusion: AppLovin rallied more than 11% after S&P Dow Jones Indices announced it will replace Caesars Entertainment in the S&P 500 on 22 September.

- Rapport Therapeutics Soars on Positive Trial Results: Rapport Therapeutics surged more than 122% after reporting positive topline results from its RAP-219 treatment for focal onset seizures.

- Forward Industries Rockets on Digital Asset Strategy: Forward Industries jumped 54% after securing $1.65 billion in cash and stablecoin to fund a Solana-focused digital asset treasury plan.

- EchoStar Jumps on $17 Billion Starlink Deal: EchoStar climbed more than 18% after SpaceX’s Starlink agreed to buy wireless spectrum from the company in a deal worth about $17 billion.

- Uber Advances on Robotaxi Partnership: Uber rose more than 3% after announcing a partnership with Chinese autonomous vehicle firm Momenta to test robotaxis in Munich.

- Telecom Stocks Decline on Spectrum Deal Impact: T-Mobile slid more than 3% and Verizon lost over 2% as SpaceX’s spectrum purchase weighed on the sector, while SBA Communications fell more than 3% and AT&T declined over 2%.

- Summit Therapeutics Plunges on Cancer Drug Uncertainty: Summit Therapeutics slumped more than 25% after new data cast doubt on the outlook for its lung cancer treatment ivonescimab.

- Norwegian Cruise Line Slides on Debt Sale: Norwegian Cruise Line dropped more than 4% after announcing plans to issue $2.05 billion of senior notes due 2031 and 2033 through a private offering.

Wall Street’s record close, Europe’s resilience in the face of political turmoil, and Asia’s gains following leadership changes in Japan highlighted a strong start to the week, though underlying risks remain. With inflation data due in the coming days, investors are cautious about whether recent gains can be sustained. Bond markets have already shown signs of tension after last week’s surge in global yields, and the combination of stretched valuations and political uncertainty leaves scope for sharper reactions once the CPI and PPI reports are released.