Wall Street ended lower on Friday as investors booked profits into the long weekend after the S&P 500’s record close above 6,500 the day before. Concerns over inflation resurfaced with July’s core PCE showing its fastest pace since February, tempering hopes of imminent Federal Reserve rate cuts. Nvidia’s decline pressured sentiment as shares extended losses, while fresh tariff uncertainty intensified after a federal appeals court ruled most of President Trump’s global levies illegal, pausing enforcement until October pending a likely Supreme Court challenge. Even so, August closed with gains across major indices, marking a fourth consecutive monthly advance for the S&P 500.

Key Takeaways:

- Dow Posts Monthly Gain Despite Friday Decline: The Dow Jones Industrial Average slipped 92.02 points, or 0.20%, to close at 45,544.88 on Friday. Despite the dip, the index advanced more than 3% in August, supported by steady corporate earnings, though Caterpillar dragged after warning of up to $1.8 billion in tariff-related costs this year.

- S&P 500 Extends Winning Streak to Four Months: The S&P 500 ended the session down 0.64% at 6,460.26, retreating from Thursday’s all-time high above 6,500. Still, the index rose nearly 2% for August, marking a fourth consecutive monthly gain, though traders remain wary heading into September, historically the weakest month for U.S. equities.

- Nasdaq Under Pressure From Tech Losses: The Nasdaq Composite shed 1.15% to finish at 21,455.55, trimming its August gain to 1.6%. Nvidia fell more than 3% after reports Alibaba had developed a new advanced chip amid U.S. export restrictions, while Dell and Super Micro Computer also slipped, adding to caution in the tech sector.

- Europe Markets End Lower on Inflation Jitters: The Stoxx 600 fell 0.6% on Friday, pressured by banking stocks as UK lenders slumped on fresh concerns over a potential windfall tax. NatWest sank nearly 5%, while Barclays lost 2.8% and Lloyds 1.2%. France’s CAC 40 declined 0.66%, Germany’s DAX lost 0.57%, and Italy’s FTSE MIB shed 0.59%. Inflation data were mixed, with France cooling to 0.8% in August while German CPI rose to 2.1% and Spain’s EU-harmonised inflation held at 2.7%. German unemployment surpassed 3 million in unadjusted terms, underscoring labour-market strains.

- Asia-Pacific Markets Mixed on Data and Politics: Asian equities diverged on Friday as investors digested Japan’s inflation slowdown and regional political developments. Tokyo’s core CPI eased to 2.5% year on year, still above the Bank of Japan’s 2% target, while unemployment dropped to 2.3%. The Nikkei 225 lost 0.26% and the Topix 0.47%. South Korea’s Kospi fell 0.32% after the indictment of former first lady Kim Keon Hee, while the won weakened slightly. By contrast, Hong Kong’s Hang Seng gained 0.45% and China’s CSI 300 rose 0.74%. India prepared for the SCO summit in Tianjin, where Prime Minister Modi and President Xi may hold rare bilateral talks.

- Oil Slips on Demand Concerns and Ceasefire Hopes: Brent crude fell 0.73% to $68.12 a barrel and WTI dropped 0.91% to $64.01 as traders looked to weaker U.S. demand at the end of the summer driving season and speculation over progress toward a Ukraine ceasefire. OPEC+ output increases and forecasts of Brent sliding to $63 in Q4 added to pressure, though U.S. inventories showed stronger late-summer draws.

- US Core PCE Rises With Services Still Firm: Core PCE rose to 2.9% in July, matching expectations but marking the fastest pace since February. On a monthly basis, core PCE increased 0.3%, while headline PCE ran at 2.6% year on year and 0.2% month on month, while goods were up 0.5% y/y and down 0.1% m/m. Energy fell 2.7% y/y and 1.1% m/m, and food rose 1.9% y/y but slipped 0.1% m/m, leaving inflation still above the 2% target even with goods and energy softness.

- Yields Edge Up After In-Line PCE: US Treasury yields firmed modestly, with the 10-year around 4.23% and the 30-year near 4.93%, reflecting unease over sticky services inflation even as markets continue to price the possibility of Fed easing next month.

FX Today:

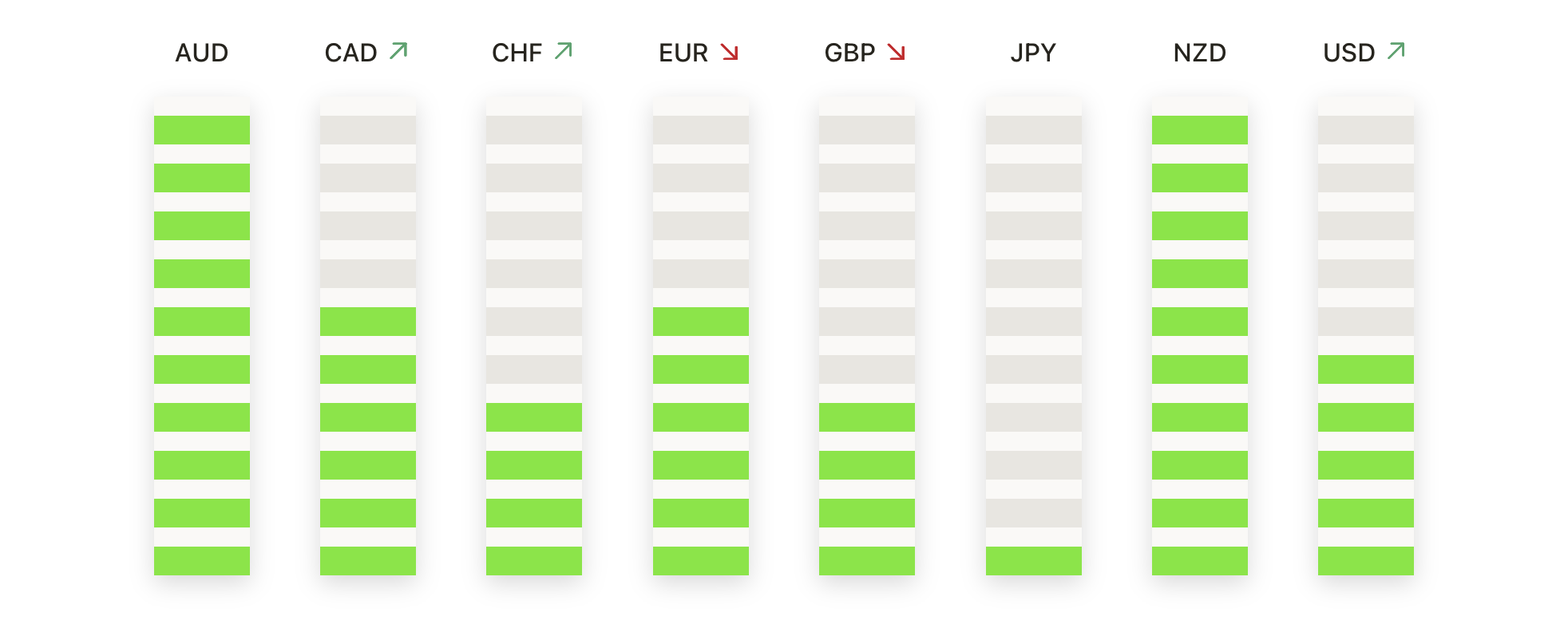

- EUR/USD Holds Firm as Buyers Build Support Above 1.1650: EUR/USD closed at 1.1700, up 0.14% after trading between 1.1651 and 1.1709. The pair extended its gradual rebound this week, with demand holding firm just above the 50-day SMA at 1.1663 and the broader bullish structure reinforced by the 100-day and 200-day averages at 1.1512 and 1.1035. Price action has carved out higher lows since dipping below 1.1550 in mid-August, reflecting steady accumulation. Despite momentum being capped near 1.1720, the constructive tone remains intact above 1.1660 and especially 1.1600. A decisive break above 1.1720 would reassert bullish control and open the way toward 1.1800, while a close under 1.1650 could undermine sentiment and re-expose 1.1550.

- GBP/USD Stabilises as Buyers Defend Ground Above 1.3500: GBP/USD ended almost flat at 1.3514, up 0.01% after ranging between 1.3445 and 1.3517. The pair consolidated above the 50-day SMA at 1.3497, while the 100-day at 1.3447 continues to underpin a constructive setup alongside the 200-day at 1.3044. The rebound from August’s trough near 1.3150 has re-established an upward bias, even if momentum remains restrained. Buyers are defending the 1.3450–1.3440 area, with deeper support at 1.3400, while resistance is layered at 1.3550–1.3600. A clear move above 1.3550 would strengthen the recovery and target 1.3650, but a failure to hold 1.3440 would risk turning attention back toward 1.3350.

- USD/JPY Holds Steady as Price Balances on Key Averages: USD/JPY closed little changed at 146.96, up just 0.02% after trading between 146.76 and 147.41. The pair continues to hover around the 50-day SMA at 146.98, while the 100-day at 145.52 and the 200-day at 148.89 frame a finely balanced backdrop. Recent consolidation follows rejection from the 151.00 region earlier in August, with the market showing no clear directional bias. Support is forming at 146.50 and 146.00, while resistance remains capped at 147.50. A decisive break above 147.50 would reinstate bullish momentum and pave the way to 148.50, whereas a drop below 146.00 could hand control back to sellers and expose 145.00.

- Silver Breaks Higher as Bulls Drive Price Toward $40: Silver closed at $39.72, gaining 1.83% after swinging between $38.73 and $39.97. The strong green candle confirmed accelerating momentum, with price surging past resistance at $39.50 and positioning just below the key $40 psychological barrier. The 50-day SMA at $37.67 underpins support alongside the broader uptrend reinforced by the 100-day at $35.67 and the 200-day at $33.48. Structurally, the latest breakout strengthens bullish conviction, with a sustained move through $40 expected to open the way toward $40.50. Immediate support now lies at $39.00, and failure to hold this level could briefly stall momentum, though the wider bias remains firmly to the upside.

- Gold Extends Rally as Buyers Push Toward $3,450: Gold climbed to $3,446 on Friday, up 0.89% after moving between $3,404 and $3,454, closing out August with a gain of more than 4.5% for its strongest monthly performance since April. The advance was underpinned by renewed rate-cut expectations following July’s inflation data, with the non-yielding asset benefiting from the prospect of lower borrowing costs. Momentum has accelerated since breaking above the 50-day SMA at $3,350 earlier this week, with the metal now comfortably supported by the 100-day at $3,326 and the 200-day at $3,060. Structurally, the push through the $3,380–$3,360 zone has re-established an upward bias, with resistance at $3,450 now being tested. A sustained break would likely target $3,475, while support rests at $3,420 and then the $3,380 breakout area, where failure to hold could stall the rally and shift focus back to the 50-day average.

Market Movers:

- Alibaba Surges on Chip Breakthrough as Nvidia Falls: Alibaba shares jumped more than 13% after reports it developed a new advanced chip to counter US export restrictions, while Nvidia slid over 3% as investors weighed risks following its strong earnings earlier in the week.

- Dell Leads Tech Decliners on Soft Income Miss: Dell Technologies tumbled more than 8% after posting Q2 operating income of $2.28 billion, missing the $2.30 billion consensus. The weakness also brought Super Micro Computer down 5% and Hewlett Packard Enterprise losing over 2%.

- Ulta Beauty Sinks Despite Beating Sales Forecasts: Ulta Beauty dropped more than 7% even as it reported stronger-than-expected Q2 net sales.

- Caterpillar Slides as Tariff Costs Mount: Caterpillar fell more than 3% after warning that tariffs could deliver a hit of up to $1.8 billion this year, making it one of the Dow’s biggest laggards and highlighting the pressure from renewed trade tensions.

- Healthcare Stocks Rally on Defensive Bid: Managed care names advanced, with Molina Healthcare gaining more than 3% and UnitedHealth up over 2% to lead Dow gainers. Elevance Health, Centene, Humana and CVS also rose as investors rotated toward defensive sectors.

- Autodesk and Ambarella Lead Gainers on Strong Results: Autodesk climbed more than 9% after beating Q2 revenue forecasts and guiding higher for Q3, while Ambarella surged 16% after delivering EPS well ahead of consensus and lifting its 2026 growth outlook to 31–35%.

- Crypto-Linked Stocks Weaken as Bitcoin Hits 7-Week Low: Bitcoin’s more than 3% slide weighed on cryptocurrency-exposed names, with Galaxy Digital down over 4% and Coinbase and MicroStrategy both losing more than 1%.

Wall Street closed out August with a pullback, as investors locked in gains after a record-setting week and assessed the implications of firmer inflation and tariff uncertainty. Nvidia’s slide, the court ruling against Trump’s trade levies, and warnings from companies such as Caterpillar weighed on sentiment, but the S&P 500 still secured a fourth straight monthly advance. With September carrying a history of weaker performance, attention now shifts to US jobs data and the Federal Reserve’s policy outlook. Markets will be closed on Monday for the Labour Day holiday before trading resumes in a new month.