US markets came under heavy pressure on Monday as renewed concerns over artificial intelligence disruption combined with fresh trade uncertainty to drive a sharp risk-off move. The Dow suffered a steep decline as investors reassessed the impact of rapid AI adoption on corporate earnings, employment, and traditional business models, while President Donald Trump’s renewed push to raise global tariffs added another layer of uncertainty. Losses were concentrated in software, financials, and cyclical sectors, with defensive areas offering only limited shelter as volatility returned across equities, bonds, commodities, and digital assets.

Key Takeaways:

- Dow Jones Slides on AI and Tariff Shock: The Dow Jones Industrial Average plunged 821.91 points, or 1.66%, to close at 48,804.06 as renewed fears over artificial intelligence disruption combined with escalating tariff threats to drive a sharp risk-off move. Heavy losses in IBM and financial stocks weighed on the index, with investors reassessing the implications of rapid AI adoption for employment, earnings visibility, and traditional business models. Trump’s renewed push to raise global tariffs added further pressure, undermining sentiment and accelerating the sell-off.

- S&P 500 Falls Back Into the Red for 2026: The S&P 500 declined 1.04% to end at 6,837.75, slipping back into negative territory for the year as broad-based selling swept across sectors. Technology and financials led the losses, while defensive pockets offered only limited protection. Investors remained cautious over the combined impact of AI-led disruption and renewed trade uncertainty on corporate profitability and growth expectations.

- Nasdaq Hit by Software and AI Exposure: The Nasdaq Composite dropped 1.13% to 22,627.27, with software stocks firmly in focus as AI disruption fears resurfaced. Microsoft fell 3%, while CrowdStrike slumped nearly 10%, reflecting concerns that rapid advances in AI tools could undermine demand for established software models. Weakness extended beyond technology into logistics, commercial real estate, and financial services.

- European Markets Slide as Tariff Risks Return: European equities closed mostly lower as markets reacted to Trump’s latest tariff escalation, with the pan-European Stoxx 600 provisionally down nearly 0.5%. The FTSE 100 slipped 6 points, or 0.05%, to close at 10,681, while France’s CAC 40 fell 17 points, or 0.20%, to 8,499 and Germany’s DAX dropped 269 points, or 1.06%, to 24,992. Italy’s FTSE MIB bucked the broader tone, rising 226 points, or 0.49%, to 46,699. Germany’s Ifo Business Climate Index improved to 88.6 in February 2026, its highest since August 2025 and slightly above the 88.4 forecast, as the current conditions gauge rose to 86.7 from 85.7 and the expectations component advanced to 90.5 from 89.6. Even with the stronger survey read, the political backdrop remained a drag after the European Parliament announced it has paused work on ratifying the US–EU trade agreement in response to the new tariff stance.

- Asia Markets Show Mixed Performance as Tariff Risks Linger: Asia-Pacific markets finished mixed but broadly resilient despite renewed global tariff uncertainty. South Korea’s Kospi surged 1.7% to a fresh record high, supported by strong gains in index heavyweights, with SK Hynix rising more than 3% and Samsung Electronics adding over 2%, while the Kosdaq advanced 0.74%. Hong Kong’s Hang Seng jumped more than 2%, extending recent momentum. Australia’s S&P/ASX 200 fell 0.6% to close at 9,026, weighed down by losses in technology, real estate, and energy stocks, while New Zealand equities rebounded sharply, gaining 112 points, or 0.8%, to finish at 13,420 after declining 1.0% in the prior session. Markets in China and Japan were closed for a holiday. In India, the BSE Sensex rose 0.58% to 83,294.66, while the Nifty 50 gained 0.55% to 25,713, though gains were capped by ongoing pressure on IT shares amid persistent AI disruption concerns.

- Oil Prices Steady as Geopolitics Offset Tariff Uncertainty: Oil prices were little changed as easing geopolitical tensions balanced concerns about global growth. Brent crude slipped 0.29% to $71.55 a barrel, while WTI edged down 0.08% to $66.42. Markets weighed the prospect of renewed US–Iran nuclear talks against the potential demand impact of higher global tariffs.

- Treasury Yields Fall as Risk Aversion Rises: US Treasury yields declined as investors sought safety amid equity market turbulence and tariff uncertainty. The 10-year yield fell more than 5 basis points to 4.031%, while the 2-year yield dropped to 3.44% and the 30-year yield eased to 4.70%, reflecting growing caution over the macro outlook.

FX Today:

- EUR/USD Holds Firm Above Key Support: EUR/USD edged higher, closing at 1.1789, up 0.04%, after trading between 1.1774 and 1.1834. The pair held above the 50-day moving average at 1.1772, reinforcing near-term support despite waning momentum near the 1.1900 area. The broader recovery structure remains intact, underpinned by higher lows since late 2025 and firm positioning above the 100-day and 200-day averages at 1.1689 and 1.1650. Resistance is seen first at 1.1834 and then near the recent swing high around 1.1920, while a sustained move below 1.1772 would expose a deeper pullback toward the 100-day average.

- GBP/USD Consolidates Below 50-Day Average: Sterling closed modestly higher at 1.3492, up 0.10%, after a range-bound session between 1.3475 and 1.3535. Price remains capped below the 50-day moving average at 1.3529, reflecting hesitation following the recent pullback from January highs. Support continues to hold near 1.3475 and the 200-day average at 1.3444, helping preserve the broader recovery trend established since October. A daily close above 1.3535 would improve the short-term outlook, while a break below 1.3475 would shift focus toward the 100-day average at 1.3393.

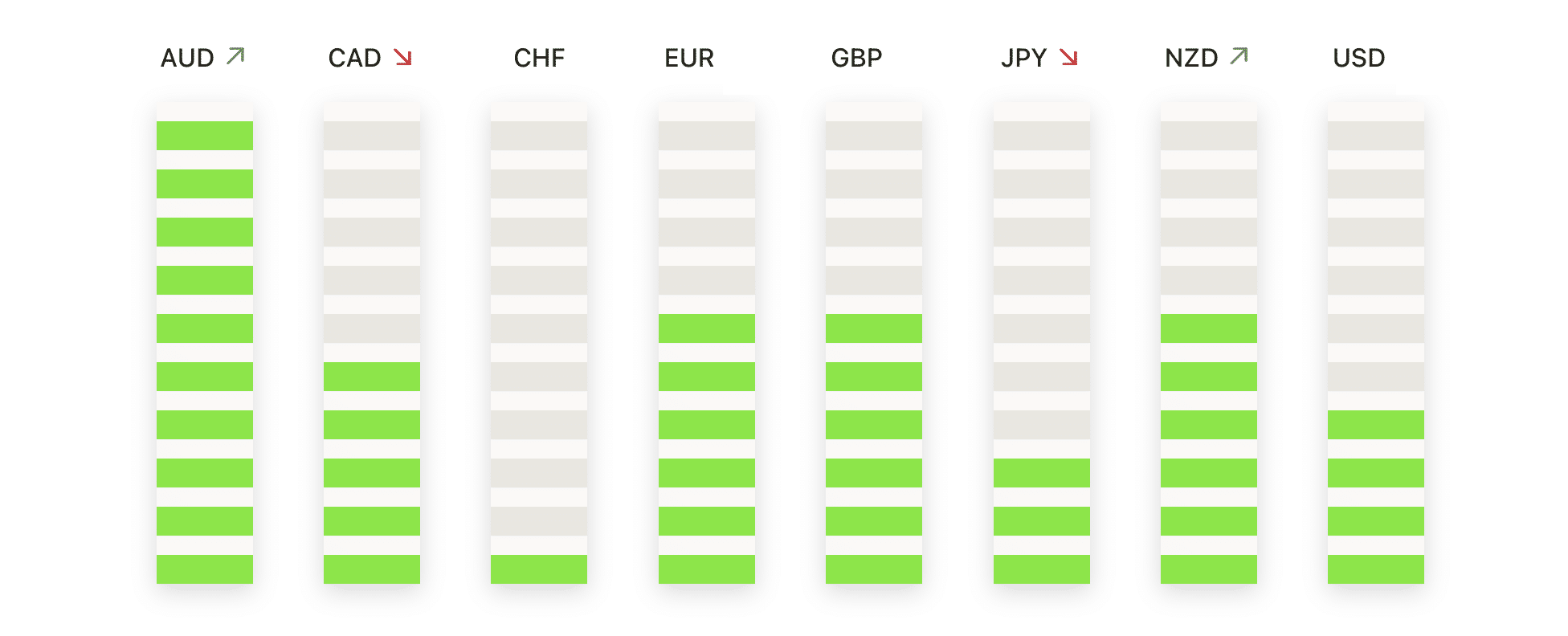

- AUD/USD Pulls Back From Recent Highs: The Australian dollar slipped 0.34% to close at 0.7056 after failing to sustain gains above 0.7100. Selling pressure emerged after the pair tested a session high of 0.7111, though price remains comfortably above the 50-day, 100-day, and 200-day averages, signalling that the broader uptrend remains intact. Immediate support is seen near 0.7048 and then around 0.6970, while resistance remains layered at 0.7111 and 0.7150. The pair appears to be entering a consolidation phase following a strong multi-month rally.

- USD/JPY Stabilises After Recent Pullback: USD/JPY closed lower at 154.70, down 0.21%, after trading between 153.99 and 155.04. The pair continues to stabilise above the 154.00 handle after a sharp pullback from multi-year highs, though price remains below both the 50-day and 100-day averages at 155.92 and 154.90. Support near 153.99 has so far limited downside pressure, while resistance is firmly set at 155.04 and the 50-day average. A recovery above these levels would signal renewed upside momentum, while a break below 153.99 would deepen the corrective phase.

- Gold Extends Rally as Safe-Haven Demand Builds: Gold surged 2.51% to close at $5,236 after breaking decisively above recent consolidation highs. The metal traded between $5,099 and $5,237, with strong buying interest pushing prices further into uncharted territory. Gold remains well supported above its 50-day, 100-day, and 200-day averages, reinforcing the strength of the longer-term uptrend. Initial support is now seen near $5,099 and then around $5,000, while further upside remains open if prices hold above the recent breakout.

- Silver Breaks Higher With Strong Momentum: Silver jumped nearly 5% to close at $88.83, extending its powerful rally after breaking above the $88.00 level. The session range between $84.56 and $89.03 highlighted strong intraday demand, with prices holding well above all major moving averages. Momentum remains firmly to the upside following February’s brief pullback, with support now seen near $84.56. A sustained close above $89.03 would confirm further upside potential, while any pullback is likely to attract buying interest.

Market Movers:

- Novo Nordisk and Eli Lilly Diverge After Trial Results: Novo Nordisk shares sank 16% after its obesity drug CagriSema failed to match Eli Lilly’s competing treatment in a recent clinical trial. In contrast, Eli Lilly shares climbed nearly 5%, as investors welcomed the comparative strength of its weight-loss portfolio.

- IBM and Cybersecurity Stocks Slump on AI Automation Fears: IBM shares closed down nearly 13.2% at $223.35 after Anthropic said its Claude Code product could automate complex analysis and exploration work central to COBOL modernisation, a key IBM business line. The sell-off rippled through cybersecurity names, with the Global X Cybersecurity ETF dropping 4%, CrowdStrike and Zscaler tumbling around 10%, and Fortinet and Okta sliding more than 5%.

- Arcellux Jumps on Gilead Takeover Deal: Arcellux surged more than 77% after Gilead Sciences agreed to acquire the biotech firm for $7.8 billion, or $115 per share, marking one of the largest healthcare deals of the year and sparking renewed interest across the sector.

- PayPal Rallies on Takeover Speculation: PayPal Holdings rose more than 5% to lead gainers in the S&P 500 and Nasdaq 100 after reports suggested the payments group has attracted takeover interest from several potential buyers.

The trading session was defined by a sharp pivot away from growth-sensitive assets as the dual threats of trade protectionism and AI-induced structural unemployment took centre stage. With the White House’s 15% global tariff policy set for immediate implementation, investors are bracing for a period of heightened volatility and potential retaliatory measures from major trading partners. In the coming days, market participants will closely monitor the progress of US-Iran nuclear talks and any further clarity on the legal standing of the administration’s trade executive orders.