Stocks advanced on Wednesday as a surprise decline in US private payrolls strengthened expectations that the Federal Reserve will cut interest rates at next week’s meeting. The softer labour data boosted confidence that monetary policy is set to ease further, helping major US indices extend recent gains despite mixed economic signals elsewhere. Financial stocks outperformed as traders positioned for a lower-rate environment, while bitcoin’s rebound added another layer of optimism across risk assets.

Key Takeaways:

- Dow Rallies on Softer Labour Data: The Dow Jones Industrial Average climbed 408.44 points, or 0.86%, to close at 47,882.90 as a surprise decline in private payrolls strengthened conviction that the Federal Reserve will cut rates next week.

- S&P 500 Edges Higher: The S&P 500 gained 0.30% to finish at 6,849.72, supported by strength across financial stocks and pockets of resilience in US services activity. While the broader market held a firmer tone, gains were limited as traders weighed the implications of weaker labour data against signs of underlying economic steadiness.

- Nasdaq Posts Modest Advance: The Nasdaq Composite rose 0.17% to close at 23,454.09, marking a subdued performance as investors balanced the rate-cut narrative with sector-specific moves in technology. Cryptocurrency-linked stocks added upward pressure as bitcoin extended its recovery from Monday’s sharp decline.

- Europe Markets Mixed but Finish Higher: European equities ended modestly higher, with the Stoxx 600 up nearly 0.1% as investors balanced softer macro signals with improving global sentiment. The FTSE 100 slipped 0.10% to 9,692.07, while France’s CAC 40 gained 0.2% as traders awaited fresh guidance from ECB officials on the path for interest rates. Germany’s DAX hovered near the flatline around 23,693 after PMI data showed services growth easing to 53.1 from October’s 29-month high of 54.6, though still signalling expansion. Switzerland’s inflation slowed unexpectedly to zero, undershooting expectations and fuelling speculation that the SNB may opt for further rate cuts next week. Spain reported a record 9.2 million international tourists in October, despite its services PMI slipping from a ten-month high to 55.6. France’s services sector returned to growth at 51.4, while Italy’s jumped to 55.0, its strongest pace in over two years. Corporate action also influenced sentiment, with Hugo Boss shares dropping nearly 10% after updated guidance pointed to a challenging 2026.

- Asia Stocks Gain as Tech Strength Leads: Asian markets delivered a broadly constructive session, led by sharp gains in Japanese technology names after Wall Street’s rebound in US peers. The Nikkei 225 rose 1.14% to 49,864.68, supported by a more than 6% jump in SoftBank and strong advances across semiconductor-related stocks including Tokyo Electron, Lasertec, Renesas and Advantest. South Korea’s Kospi climbed 1.04% and the Kosdaq added 0.39%, aided by upgraded Q3 GDP figures showing 1.8% year-on-year growth. Australia’s ASX 200 gained 0.18% despite Q3 GDP missing expectations, with the economy still recording its strongest expansion in nearly two years. By contrast, Hong Kong’s Hang Seng fell 1.28% and China’s CSI 300 slipped 0.51% amid continued weakness in mainland sentiment. India’s Nifty 50 and Sensex also retreated, while the rupee weakened for a fifth straight day to 90.157.

- Oil Prices Rise: Brent crude rose 0.61% to $63.81 and WTI added 0.84% to $59.13 after Moscow–Washington peace talks failed to produce progress, lowering hopes of sanctions relief for Russian oil. US inventory data from the API showed increases across crude and gasoline.

- Treasury Yields Decline: The 10-year Treasury yield fell more than 2 basis points to 4.059%, while the 2-year yield slid to 3.486%, as the ADP report reinforced expectations of a third Fed rate cut this year. Bond markets strengthened on rising confidence that policymakers will lower rates by another quarter point next week.

- US Private Payrolls Fall: ADP data showed private payrolls declined by 32,000 in November, defying expectations for a 40,000 increase and reversing October’s upwardly revised 47,000 gain. The weak reading added to signs of labour-market cooling, though economists noted that ADP figures can diverge from official BLS data. Separately, US import prices were unchanged in September, masking divergent movements across energy, consumer goods and food categories.

FX Today:

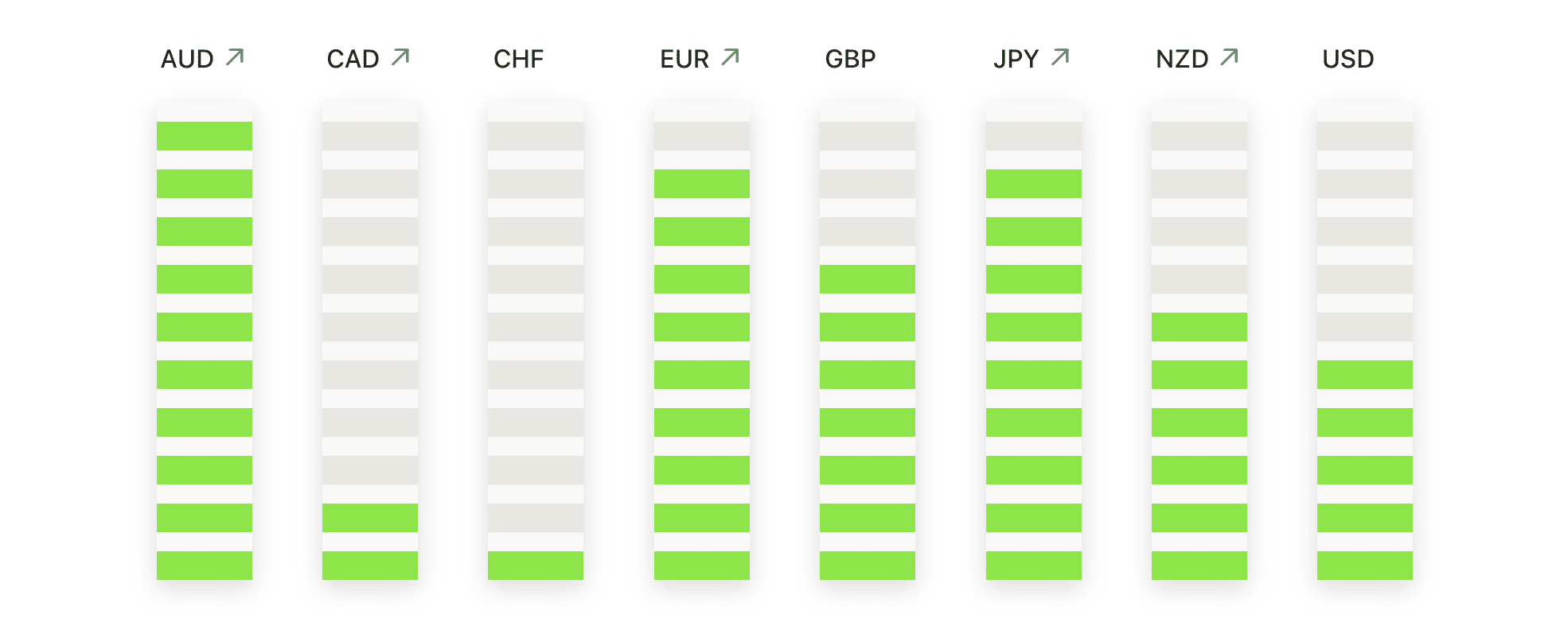

- EUR/USD Pushes Higher as Buyers Reclaim Key Levels: EUR/USD closed at 1.1666, up 0.36%, after trading between 1.1678 and 1.1621, ending near the top of the day’s range as upside interest strengthened. The pair continued to build momentum above the 50-day SMA at 1.1617 and the 100-day SMA at 1.1644, both turning higher, while the 200-day SMA at 1.1450 remains a firm base for the broader uptrend. Price has recovered steadily from late-November lows and has now moved beyond the 1.1620 zone, which flips to immediate support as the pair approaches the late-October high. Resistance is located at 1.1678 and then near 1.1710, with scope for further gains if bullish control persists. A drop back below 1.1617 would soften the near-term tone and risk a deeper pullback toward 1.1580.

- GBP/USD Jumps Sharply as the Pair Retakes Major Averages: GBP/USD settled at 1.3348, up 1.02%, after moving between 1.3353 and 1.3206, producing a strong bullish candle that overwhelmed the previous session’s action. The rally propelled the pair above the 50-day SMA at 1.3268 and the 200-day SMA at 1.3322, putting the 100-day SMA at 1.3369 as the next key hurdle. This latest move challenges the downward sequence seen through November and signals a renewed upside phase following a firm rebound from the 1.3000 area. Resistance is now at 1.3369 and 1.3400, while support sits at 1.3322 and then 1.3288. A clear break above 1.3369 would open the door toward 1.3500, whereas slipping below 1.3322 risks a pullback toward the 50-day average.

- EUR/GBP Slides as the Cross Breaks Beneath the 50-Day Average: EUR/GBP closed at 0.8739, down 0.59%, after trading between 0.8799 and 0.8737, finishing near the session low as selling pressure intensified. The move took the pair decisively below the 50-day SMA at 0.8749, shifting the short-term tone more bearish while the 100-day SMA at 0.8708 and 200-day SMA at 0.8591 remain supportive on a broader horizon. The break under the recent support zone places focus on the 0.8737 low and then the 100-day SMA, both key areas for buyers attempting to maintain the wider uptrend. Resistance now stands at 0.8749 and the 0.8760 region, with recovery prospects weakening should the pair fail to reclaim those levels.

- USD/JPY Pullback Continues as the Pair Retreats from Recent Highs: USD/JPY finished at 155.23, down 0.40%, after ranging between 155.90 and 155.01, closing near the day’s low as the corrective move persisted. Despite the decline, the pair remains well above the 50-day SMA at 152.98, the 100-day SMA at 150.33 and the 200-day SMA at 148.06, all aligned with a dominant long-term uptrend. The pullback follows a rally toward the 157.80 high, with the 155.00 psychological area now acting as a potential stabilisation point. Support rests at 155.01 and then 152.98, while resistance is seen at 156.40 and 157.80. Holding above 155.01 would signal consolidation, whereas a deeper break could point to an extended correction.

- AUD/USD Extends Rally as Momentum Builds Above Key Support: AUD/USD closed at 0.6601, up 0.60%, after trading between 0.6602 and 0.6562, ending near the session high as bullish momentum strengthened. The pair now trades comfortably above the 50-day SMA at 0.6529, the 100-day SMA at 0.6533 and the 200-day SMA at 0.6466, supporting a constructive outlook following the late-November rebound. The breakout above 0.6580 has shifted the near-term structure upward, placing attention on resistance at 0.6602 and the late-September high near 0.6630. Support is now at 0.6580 and then 0.6533, with a sustained move above today’s high likely to extend the recovery toward 0.6680.

Market Movers:

- Crypto-Linked Stocks Rise with Bitcoin Rebound: Cryptocurrency-exposed equities strengthened as bitcoin climbed more than 1% to a two-week high. Galaxy Digital advanced over 6%, Coinbase gained more than 5%, MARA Holdings rose more than 4%, and Strategy and Riot Platforms added more than 3% and 2%, respectively.

- Microsoft Slips on AI Quota Concerns: Microsoft declined 2.5% after reports suggested the company was cutting sales quotas tied to artificial intelligence.

- Pharvaris Surges on Trial Success: Pharvaris shares jumped more than 21% after announcing that its late-stage study of an investigational hereditary angioedema therapy achieved its primary endpoint, supporting confidence in its clinical trajectory.

- American Eagle Jumps on Strong Revenue: American Eagle Outfitters climbed more than 14% after reporting Q3 revenue of $1.36 billion, above estimates of $1.32 billion.

- Pure Storage Drops on Disappointing Outlook: Pure Storage sank more than 27% after issuing Q4 operating-income guidance of $220–$230 million, slightly above estimates.

- GitLab Falls on Revenue Forecast: GitLab slid more than 13% after projecting Q4 revenue of $251–$252 million, with the midpoint coming in below consensus expectations.

US equities extended their upward momentum on Wednesday as investors interpreted the unexpected drop in ADP private payrolls as further confirmation that the Federal Reserve is on course to cut rates next week. Financials and rate-sensitive names benefited most from the shift in expectations, while global markets broadly echoed the constructive tone, supported by improving European data and strong gains across Asia’s tech sector. Bitcoin’s recovery above $93,000 added an additional boost to risk appetite, reinforcing the sense that markets are positioning for a more supportive policy environment heading into the final stretch of the year.