Despite a promising start to the trading day, major US stock indexes weakened, marking a continued decline amid tech sector struggles and mixed global economic signals. The S&P 500 and Nasdaq Composite closed lower for the fourth consecutive day, influenced heavily by a notable slide in Nvidia shares and a disappointing performance across other major technology firms. Investors, initially lifted by some positive earnings surprises earlier in the season, are increasingly cautious as they deal with a string of less favourable financial outcomes and statements from key economic leaders that hint at ongoing challenges. This restraint reflects a broader hesitancy in the markets, with a shift in focus towards potentially more stable sectors.

Key Takeaways:

- Continued Decline in Major Indices: The S&P 500 dropped by 0.58%, while the Nasdaq Composite fell more significantly by 1.15%. The Dow Jones Industrial Average experienced a more modest decline, decreasing by 45.66 points or 0.12%, indicating a broader market unease despite initial gains during the session.

- European Markets Close Higher Amid Global Uncertainty: European stocks defied broader market trends and closed higher, with the Stoxx 600 index rising by 0.2%. Notably, shares of luxury group LVMH climbed by as much as 5.2%, reflecting a robust performance in the luxury goods sector despite cautious market sentiment.

- Mixed Performance in Asian Markets: Asian markets showed a mixed response; Japan’s Nikkei 225 decreased by 1.32%, marking a significant drop below the 38,000 level. However, the CSI 300 in China rose by 1.55%, indicating some optimism in the region despite broader sell-offs across Asia.

- Tech Sector Faces Significant Struggles: Notable technology companies like Nvidia saw a significant decrease, with shares falling over 3%. This downward trend was echoed by other major tech players such as Netflix, Meta, Apple, and Microsoft, leading to tech becoming the worst-performing sector in the S&P 500 with a drop of more than 1%.

- Oil Prices Slide Amid Geopolitical Tensions: Crude oil futures experienced a significant drop, with US West Texas Intermediate falling over 3% to settle at $82.69 a barrel. This movement reflects market reactions to diminishing concerns over a potential escalation between Israel and Iran, despite the ongoing geopolitical tensions in the region.

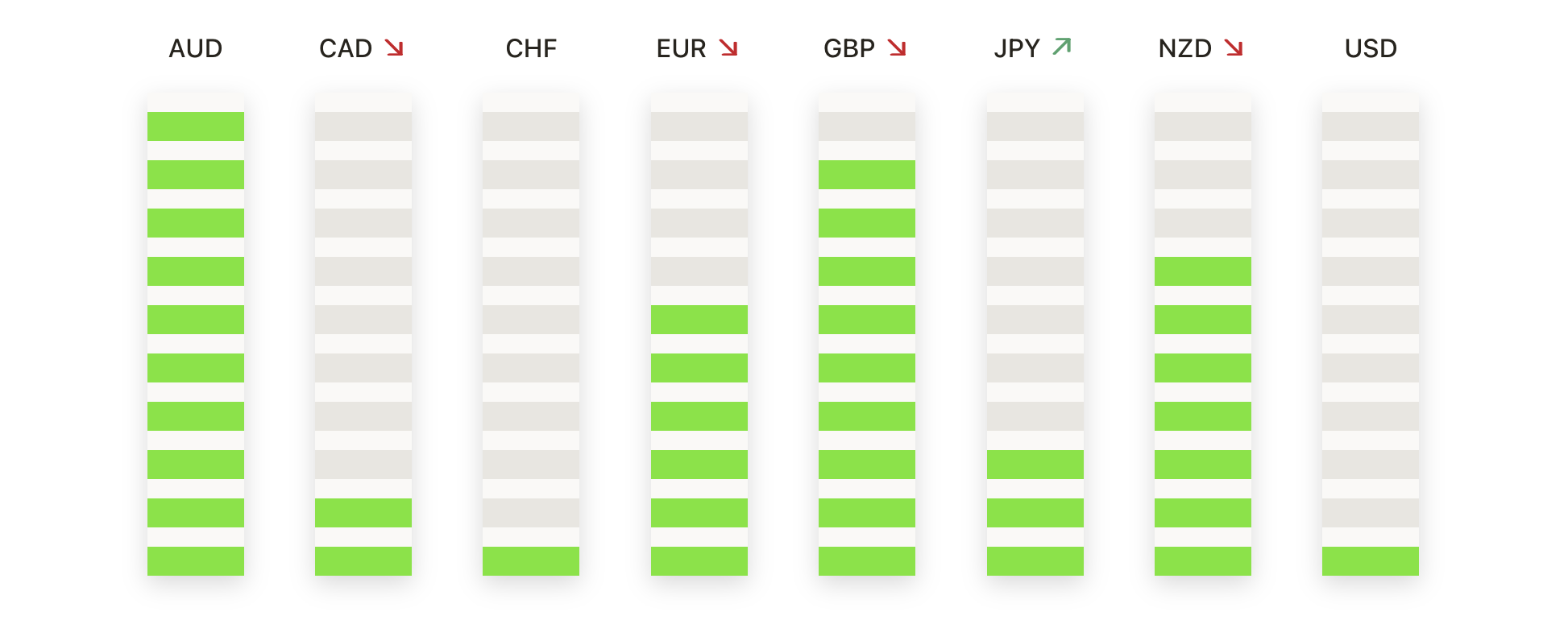

FX Today:

- GBP/USD Gains Ground After British Inflation Data: The GBP/USD pair is currently trading slightly higher at 1.2448, marking modest gains. The slight uptick follows UK inflation data which came in at 3.2%, sparking concerns over U.S.-style price stickiness. This data has influenced market expectations regarding the timing of the Bank of England’s future rate cuts, contributing to the current trading dynamics of the pair.

- USD/CAD Tests Support Amid Rate Cut Speculations: The USD/CAD pair showed some movement, trading at 1.3779 after touching a nearly 6-month low. This reflects increasing bets that the Bank of Canada might cut rates in the coming months, in contrast to a potentially more hawkish Federal Reserve. These dynamics are reshaping the trading patterns for the USD/CAD pair.

- USD/JPY Maintains Position Amid Central Bank Outlook: The USD/JPY traded defensively but managed well to keep the trade north of 154.00. Recent remarks by Bank of Japan officials hint at a cautious approach to Japan’s monetary policy, affecting the pair’s performance as investors gauge the implications for currency valuations.

- Gold Prices Adjust Amid Market Volatility: Gold prices saw a notable adjustment, retreating to approximately $2,370, down from a recent high near $2,400. The pullback suggests a moderating of investor sentiment towards safer assets. Besides this dip, gold’s trading range for the week was between $2,350 and $2,400, reflecting continued volatility and the market’s sensitivity to both domestic and international economic cues.

- Silver Price Analysis: XAG/USD Clings to Gains Above $28.00: Silver’s prices remain in positive territory but continued to register higher tails on the daily chart, signalling buyers’ failure to commit to higher prices above the May 18, 2021, high of $28.74. At the time of writing, XAG/USD trades at $28.21 and gains 0.50%. The significant $28.00 level is exposed, and a break below could lead to a retest of lower supports.

Market Movers:

- United Airlines Soars on Strong Earnings Report: United Airlines shares surged by 17.5% after the airline reported a narrower-than-expected loss for the first quarter, with quarterly revenue reaching $12.54 billion, surpassing the LSEG estimate of $12.45 billion. This significant jump underscores the market’s positive response to the travel sector’s potential rebound.

- Travelers Companies Faces Setback After Earnings Miss: Shares of Travelers Companies fell by 7.4% following a disappointing first-quarter earnings report. The company posted earnings of $4.69 per share on revenue of $10.18 billion, below analysts’ expectations of $4.90 per share on $10.51 billion of revenue. Higher-than-expected catastrophe losses played a significant role in the earnings shortfall, dampening investor sentiment.

- J.B. Hunt Transport Services Drops on Earnings Disappointment: J.B. Hunt Transport Services experienced an 8% drop in stock value after the company missed Wall Street’s quarterly expectations. The transportation firm reported earnings of $1.22 per share on revenue of $2.94 billion, missing the anticipated earnings of $1.52 per share on $3.12 billion in revenue, highlighting challenges in the logistics sector.

- Eli Lilly Holds Steady Amid Promising Drug News: Eli Lilly’s shares remained stable even as the company announced promising results for its Zepbound weight loss drug in treating patients with obstructive sleep apnea. The announcement reflects the market’s measured response to new pharmaceutical developments, with potential long-term impacts on the company’s stock.

- ASML Drops on Sales and Bookings Shortfall: Shares of ASML, the Dutch semiconductor equipment company, fell by 7.1% after the company reported that its net sales and new bookings fell short of expectations, declining about 22% year over year. The news raised concerns about the company’s performance amidst challenging global semiconductor market conditions.

- Interactive Brokers Climbs on Positive Financials: Interactive Brokers saw its shares increase by 1.7% after reporting quarterly results that slightly exceeded Wall Street’s forecasts. The firm also raised its dividend from 10 cents to 25 cents, signalling strong financial health and confidence in its operational stability.

- Autodesk’s Stock Tumbles Amid Accounting Investigation: Autodesk shares sank nearly 6% following the company’s announcement that it will delay its annual 10-K filing due to an ongoing internal investigation into some of its accounting practices. This news has raised concerns about the transparency and reliability of the company’s financial reporting.

- US Bancorp Lowers Guidance, Shares Fall: US Bancorp’s stock declined about 4% after the regional bank lowered its net interest income guidance for 2024, citing persistent inflation and a high-for-longer interest rate environment. This adjustment in guidance reflects broader banking sector challenges and investor wariness about future profitability.

- CSX Slightly Up After Beating Estimates: CSX Corporation saw a modest increase of about 1% in its shares after the railway company reported earnings of 46 cents per share on revenue of $3.68 billion, beating Wall Street estimates which anticipated earnings of 45 cents a share on revenue of $3.67 billion. CSX also reaffirmed its 2024 full-year guidance for revenue growth and volume, strengthening investor confidence.

- Alcoa Sees Mixed Reactions Amid Market Fluctuations: Alcoa’s stock experienced varied responses, initially dropping 1.5% after President Biden announced plans to triple the China tariff rate on aluminium and steel imports. However, the shares later climbed 2.7% after first-quarter revenue surpassed analysts’ forecasts at $2.6 billion, despite posting a wider-than-anticipated loss of 81 cents per share, versus an expected loss of 55 cents per share.

As April progresses, the downward trend in major indices such as the S&P 500 and Nasdaq reflects growing market caution, driven by tech sector volatility and mixed earnings reports. Despite some companies like United Airlines and Interactive Brokers exceeding expectations, notable declines in tech giants and mixed performances across other sectors underscore the complex challenges facing investors. This period of market adjustment highlights the balance between optimism sparked by sporadic earnings successes and the harsh reality of economic headwinds, including persistent inflation and interest rate concerns. Investors continue to balance risk with the potential for strategic gains in a changing economic environment.