The global markets showed varied trends today, with the S&P 500 barely moving as concerns over increasing bond yields tempered the enthusiasm from a solid round of corporate earnings. Despite the broader market’s passive movement, there was a slight positive note in the tech-heavy Nasdaq, contrasted by a minor retreat in the Dow. Rising bond yields continue to cause fears of interest rate hikes, overshadowing gains from corporate financial reports and creating a tense atmosphere among investors. This backdrop sets a cautious stage as all eyes turn to the upcoming economic data releases, which could significantly influence market sentiment and monetary policy directions in regions across the globe.

Key Takeaways:

- S&P 500, Dow, and Nasdaq Show Varied Movements: The S&P 500 edged up just 0.02% as rising bond yields dampened the enthusiasm from strong corporate earnings, finishing at a near-flat level due to heightened interest rate fears. The Dow Jones Industrial Average fell by 42.77 points, a decrease of 0.11%, while the Nasdaq Composite saw a marginal rise of 0.1%, signalling mixed investor sentiment across major US indices.

- European Markets Retreat Amid Disappointing Earnings and Inflation Worries: The Stoxx 600 fell by 0.43%, with key losses driven by financial services sectors that dropped 1.9% and the UK’s FTSE 100 snapping a five-day winning streak by closing 0.06% lower. Kering led the downturn among blue chips with a nearly 7% drop, severely impacting market sentiments due to forecasted operational profit challenges, particularly from its flagship brand, Gucci.

- Asian Markets Rally on Optimistic Economic Data: The Nikkei 225 in Japan led regional gains by jumping 2.42% to 38,460.08, while South Korea’s Kospi climbed 2.01% to close at 2,675.75, powered by a significant 4.11% gain in heavyweight Samsung Electronics. Australia’s S&P/ASX 200 slightly retreated after earlier gains, ending just below the flatline despite a CPI reading that suggested a continuing slowdown in inflation for a fifth consecutive quarter.

- Bond Yields Escalate: The yield on the benchmark 10-year Treasury note rose by 6.4 basis points to 4.662%, and its 2-year counterpart increased by 3.8 basis points to 4.943%, reflecting growing concerns over interest rate trends and their potential impact on equities.

- Inflation and Economic Data in Focus: With the upcoming release of key US economic data, including first-quarter GDP and the core personal consumption expenditures price index, markets are on high alert for indicators that could influence Federal Reserve policies.

- Oil Prices Fluctuate Amid Global Supply Adjustments: US crude oil hovered below $83 a barrel, with the West Texas Intermediate June contract pricing at $82.81, down 55 cents, or 0.66%. Brent crude for the June contract fell 40 cents to $88.02, reflecting a decrease of 0.45%. These price movements are influenced by increasing global oil inventories and a potential easing of geopolitical risks that could lower the oil risk premium by another $5 to $10 a barrel in the coming months.

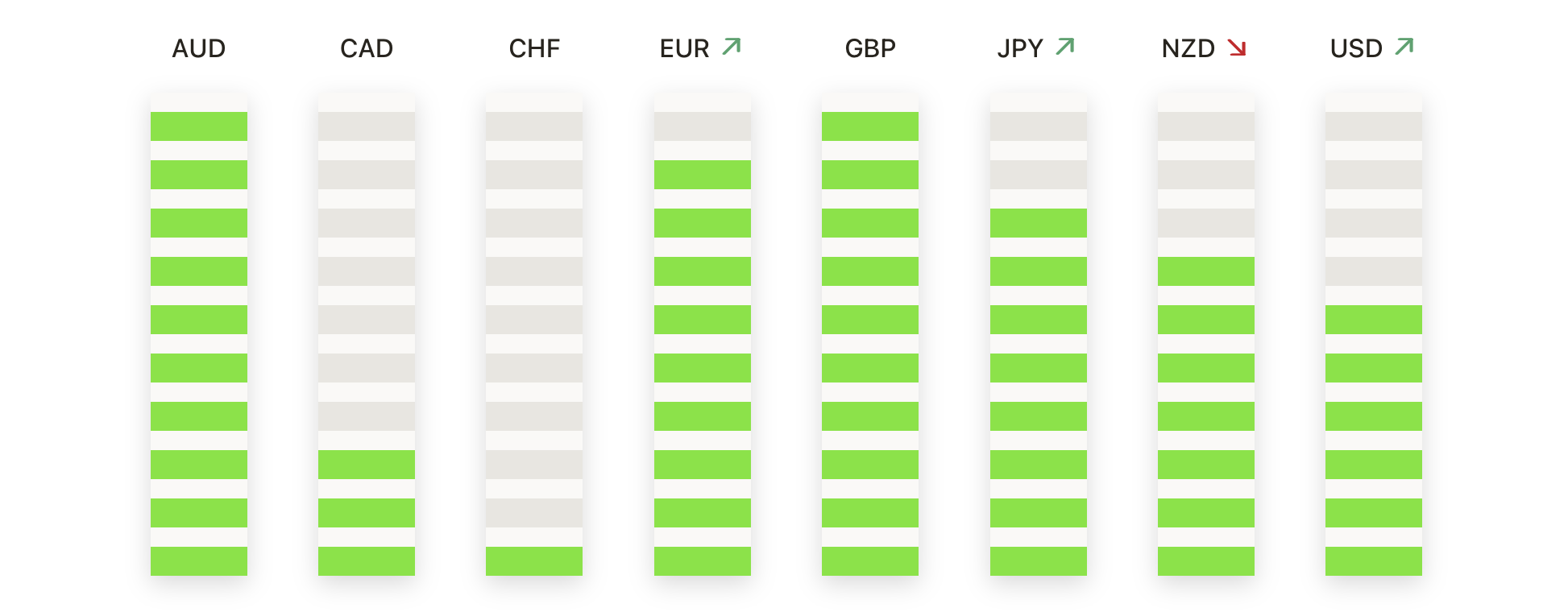

FX Today:

- EUR/USD Stabilises Amid Yield Pressures: The EUR/USD pair has shown resilience in the face of a strengthening US Dollar, influenced by elevated US Treasury yields. The pair fluctuated around the 1.0700 mark, showing modest upward momentum from a recent low at 1.0600, but it failed to breach the 1.0700 resistance decisively.

- EUR/GBP Sees Short-Term Volatility: The EUR/GBP pair experienced notable volatility last week, initially surging after the Bank of England indicated that UK inflation is trending towards its target. Looking ahead, the recent peak near 0.8645 is expected to serve as a key resistance level. Currently, the 0.8550 mark is supported by the 20-day and 50-day simple moving averages.

- USD/CAD Climbs on Retail Sales Disappointment: Following weaker-than-expected Canadian retail sales data, USD/CAD rebounded to just above the 1.3700 level. The pair tested resistance at the 200-hour Exponential Moving Average near 1.3715, reflecting renewed strength in the US Dollar against the Canadian Dollar.

- AUD/JPY Reaches Multi-Year Highs: The AUD/JPY pair surged to 101.12, its highest since 2014, propelled by bullish sentiment and a generally weaker Japanese Yen across the board. The pair later stabilised at 100.89, maintaining strong gains amid optimistic market conditions.

- JPY Weakness Continues: The USD/JPY pair escalated to a high of 155.37, the strongest since mid-1990, as the Japanese Yen continued to weaken. This move reflects growing market scrutiny over potential intervention by Japanese authorities to support the yen, with discussions of possible actions if the yen approaches the 160 level.

Market Movers:

- Tesla Surges on Model News: Tesla (TSLA) led the gainers in both the S&P 500 and Nasdaq 100, soaring more than 12% after announcing plans to accelerate the launch of less-expensive models, which overshadowed a weaker-than-expected Q1 earnings per share report.

- Meta Faces Setbacks Post-Earnings: Shares of Meta Platforms (META) plummeted over 17% in extended trading hours following a Q1 report where the company forecasted potentially up to $40 billion in capital expenditures for 2024, despite surpassing revenue estimates.

- Ford Rises on Earnings and Outlook Boost: Ford Motor (F) saw its stock climb 2% after exceeding first-quarter adjusted earnings expectations and revising its adjusted free cash flow outlook for 2024 upward, although its revenue fell short of forecasts.

- Biotech and Healthcare Excel: Biogen (BIIB) shares increased by over 4% following a Q1 report that beat earnings expectations and provided an optimistic full-year adjusted EPS forecast. Similarly, Boston Scientific (BSX) advanced more than 5% after lifting its full-year earnings outlook post-strong Q1 results.

- IBM Acquires HashiCorp, Shares Slide: International Business Machines (IBM) fell 6.6% after hours when it announced a $6.4 billion acquisition of HashiCorp, coupled with a revenue miss in its first-quarter financial results and a negative foreign exchange impact forecast.

- Semiconductor Sector Rallies: ON Semiconductor (ON), Texas Instruments (TXN), and Microchip Technology (MCHP) each closed up significantly, benefiting from Texas Instruments’ positive revenue report and Q2 revenue forecast, which beat consensus expectations and fuelled gains across the semiconductor industry.

- Westinghouse Air Brake Technologies Outperforms: Shares in Westinghouse Air Brake Technologies (WAB) jumped over 10% after reporting strong Q1 sales figures that exceeded analyst expectations and raising its full-year sales outlook.

- Old Dominion Leads Losers on Revenue Miss: Old Dominion Freight Line (ODFL) led the decline among major indices, dropping over 11% after its Q1 revenue fell below market expectations, highlighting sensitivity to even slight misses in a volatile trading environment.

- ServiceNow Dips on Earnings Beat: ServiceNow (NOW) dropped 5% despite narrowly beating analysts’ expectations for revenue in the first quarter, reflecting the market’s high expectations and sensitivity to forward-looking guidance.

- Hilton Worldwide Climbs on Strong Earnings Outlook: Hilton Worldwide Holdings (HLT) surged more than 3% after reporting a stronger-than-expected Q1 adjusted Ebitda and raising its full-year forecast, reflecting optimism in the recovery and growth of the hospitality sector.

- Masco Corporation Falls on Forecast Cut: Masco (MAS) shares fell more than 4% after reporting Q1 net sales slightly below expectations and reducing its full-year adjusted EPS forecast, which dampened investor sentiment around the company’s near-term prospects.

- General Dynamics Slides on Earnings Miss: General Dynamics (GD) experienced a drop of more than 4% after its Q1 earnings per share fell short of analysts’ expectations, underlining challenges in the aerospace and defence sector.

As the markets navigated choppy waters, the mixed performance of major indices reflected the tug-of-war between healthy corporate earnings and long-standing concerns over inflation, interest rates, and geopolitical tensions. With major stocks like Tesla and Meta driving headlines, the landscape of investment continues to evolve, influenced by both microeconomic factors and broader economic conditions. As investors digested the flood of data and corporate reports, the markets remained in a delicate balance, with every piece of new information capable of having important consequences.